Shareholder Proposals and Corporate Governance in a Season of Regulatory Uncertainty

Access the full text here.

Executive Summary

In the 2026 proxy season, the Securities and Exchange Commission (SEC) Division of Corporation Finance upended a long-standing practice of issuing informal decisions on whether shareholder proposals are excludable by the companies receiving them.

Although the SEC shareholder proposal rule, Rule 14a-8, remained in force, the SEC’s administrative dispute resolution mechanism—neutral staff review through the no-action process—was gone. The Division cited resource constraints and the sufficiency of existing guidance to justify suspending the no-action process for the current proxy season. As it stated on November 17, “due to current resource and timing considerations… as well as the extensive body of guidance from the Commission and the staff available to both companies and proponents… the Division has determined to not respond to no-action requests…” How did these changes affect the ability of shareholders to use the proposal process to raise potentially material issues with their companies and fellow shareholders? How did the SEC’s absence as a neutral arbiter of exclusion claims affect how issuers and proponents behaved? How did it affect the efficiency and effectiveness of the shareholder proposal process as a means of placing important questions before shareholders on corporate proxy statements? This analysis examines how the shareholder proposal process functioned during the 2025–2026 proxy season to identify patterns in how companies and shareholders navigated the process in the absence of routine staff review, to assess issues of fairness, balance, and efficiency and to make recommendations based on the lessons from the season.

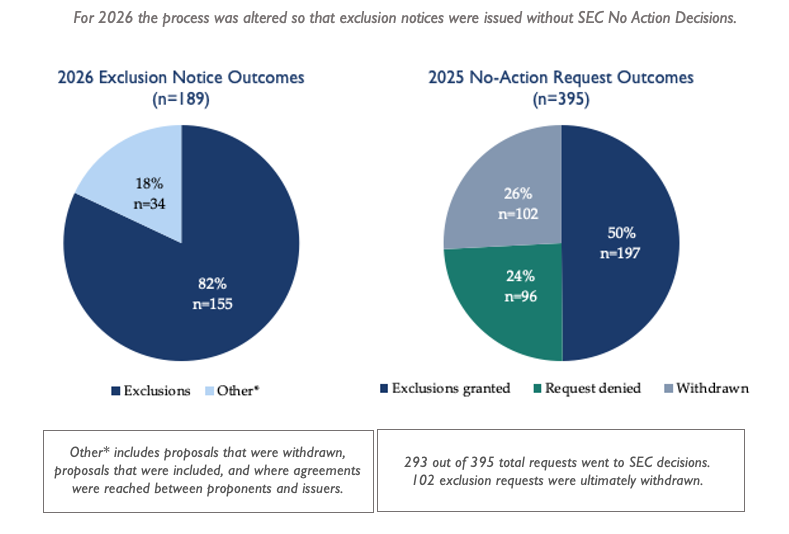

The data indicate a chilling effect on both proponents and issuers. Shareholders filed approximately 20% fewer proposals for the 2026 season. Companies filed over 100 fewer exclusion notices.

Many companies, it seems, made a prudent judgment: without SEC staff guidance on individual proposals, unilateral exclusion carried too much risk, including proponent litigation, reputational risk, potential fuel for a proxy fight over director elections, and other concerns. Rather than exploit the absence of oversight, many companies receiving proposals let the proposals go to the proxy, sometimes even explicitly citing the lack of SEC guidance as their reason for including proposals they believed might otherwise be excludable. Other companies similarly situated engaged with proponents to produce settlement agreements.

The rate at which proposals were excluded by companies in proportion to the number of proposals filed, in the absence of the SEC’s informal determinations, was similar to the rate excluded last year after SEC determinations. Yet, analysis of these exclusions revealed several important trends.

Comparison of 2025 and 2026 Process Outcomes

One of most common justifications for excluding proposals was the ordinary business rule—a determination that typically turns on subjective factors and has historically benefited from substantive SEC staff evaluation. Unfortunately, the largest portion of these exclusions clearly disadvantaged proponents who were either filing proposals on emerging risks on which staff had not previously opined or had refined a prior proposal’s language to address prior SEC staff concerns about prescriptive language. In both categories, the absence of SEC involvement undermined an orderly process and fair resolution of disputes over excludability, allowing exclusions to proceed despite the lack of staff guidance.

This exclusion trend is particularly troubling for proposals addressing an issue on which the staff has never opined. Even if the proposal concerned a significant emerging risk, exclusion could proceed despite the lack of staff guidance.

For example, at proposal at Amazon requesting company-specific disclosure of workforce risks tied to evolving U.S. immigration policy was excluded despite the absence of prior staff guidance on the topic. Proponents sought analysis of how recent and anticipated changes to immigration rules—particularly those affecting H-1B visa holders, warehouse labor, and truck drivers—could disrupt workforce, logistics capacity, and operating costs. Given the scale of Amazon’s workforce and reliance on these labor segments, this is an issue that a reasonable investor could view as financially material and decision-useful, yet the proposal was excluded without the benefit of any staff position addressing similar subject matter.

Similarly, on a year-to-year basis, the SEC sends signals to proponents and issuers regarding whether proposal language is too prescriptive, allowing proponents to revise proposals accordingly. This iterative feedback loop aligns proposal drafting with evolving staff interpretations. However, in the 2026 proxy season, such revisions were not ratified by staff review. As a result, issuers exercised unilateral discretion, and even proposals that may have been revised in good faith to conform with prior SEC guidance were nevertheless excluded.

For example, at AbbVie Inc., shareholders requested that the board oversee human rights due diligence to produce an impact assessment identifying actual and potential adverse human rights impacts in the company’s operations and supply chain, including effects on the right to health. Notably, this proposal appears to have been drafted to be less prescriptive than a prior 2025 proposal seeking a human rights impact assessment submitted to Eli Lilly, which the staff had permitted to be excluded on micromanagement grounds. The Eli Lilly proposal explicitly mandated the assessment cover “operations, activities, business relationships, and products”. By contrast, the AbbVie proposal narrowed and generalized the request—focusing on board oversight and an impact assessment framework rather than dictating exhaustive coverage parameters. Despite this apparent effort to align with prior staff reasoning and reduce prescriptiveness, AbbVie relied on the earlier Eli Lilly determination to justify exclusion. This illustrates how, in the absence of updated staff review, even materially revised proposals that address prior deficiencies can be excluded based on inapposite precedent.

Thus, an analysis of the ordinary business exclusions reveals that exclusions during this season disproportionately blocked (i) proposals addressing emerging issues lacking precedent and (ii) proposals that had undergone compliance-oriented revisions based on prior staff signals. The absence of no-action letters was therefore not neutral—it both impeded shareholders’ ability to surface new, financially relevant risks and disrupted the established corrective process that typically refines proposal language over time.

In another significant portion of exclusions, the companies claimed that their own activities substantially implemented the proposal. SEC staff is better positioned to provide a neutral evaluation of whether the company activities go as far as a proposal requests. These determinations are not appropriately left to the issuers.

Technical grounds—such as providing inadequate documentation that the proponent owned the necessary shares, or missing filing deadlines—accounted for another meaningful portion of exclusions. Some of these deficiencies seemed clear-cut. But without a structured opportunity for proponents to respond, questions remained about whether some of these technical exclusions rested on incomplete or disputed records that SEC staff would historically have scrutinized.

The disappearance of routine administrative review also caused at least six proponents to bring their disputes into federal court. Three of these cases resolved quickly after the companies agreed to include the proposals or provide the requested disclosure. These cases underscore how, in the absence of staff intermediation, formal legal action began to substitute for what had previously been an administrative and negotiated process. As proponent driven litigation became the primary enforcement mechanism for Rule 14a-8, a structural imbalance also took shape: the ability to defend a proposal increasingly depended on having the financial and legal resources to sue, in contradiction of the rule’s share ownership thresholds—which were designed to give even modest Main Street shareholders a voice.

This shift reflects a broader reconfiguration of how the rule operates in practice. Rule 14a-8 has historically depended on a combination of administrative oversight, evolving staff interpretation, and iterative dialogue between companies and investors. When the administrative layer was removed, interpretive authority shifted to issuers, and dispute resolution migrated to litigation and market pressure.

In that environment, the dynamics between proponents and companies changed materially. Proponents—who typically seek collaborative engagement with the company and dialogue with fellow shareholders—were forced into a position where they must consider escalation, including litigation, to ensure inclusion of proposals on the proxy.

The report concludes with five key recommendations for strengthening Rule 14a-8 and the shareholder proposal framework:

Preserve Rule 14a-8. The shareholder proposal mechanism is a vital communication channel between investors and corporate management. Weakening or eliminating it would undermine shareholders’ ability to raise governance concerns and hold management accountable.

Restore the no-action process. The SEC should revive its administrative process for resolving proposal exclusion disputes. Without it, conflicts are pushed into costly federal litigation or contentious shareholder campaigns. Some streamlining is possible for clear-cut procedural defects, but contested or fact-dependent claims still require meaningful staff review.

Eliminate “no-objection” letters. The practice of issuing no objection letters based solely on a company’s own unverified representations is inconsistent with Rule 14a-8’s intent. It implies administrative endorsement of unilateral exclusions regardless of consistency with the rule, and should be discontinued.

Issue clearer, more objective guidance. While appropriately restoring clarity about ensuring that proposals are relevant to the companies receiving them, Staff Legal Bulletin 14M also introduced excessive subjectivity into key exclusion determinations—particularly on “ordinary business” and “micromanagement” grounds. The subjective criteria provide staff with too much discretion; returning to more objective standards would improve predictability and reduce the need for repeated case-by-case adjudication.

Protect smaller shareholders’ access. Any reforms should ensure the process remains accessible to individual investors and smaller asset managers, who are unlikely to pursue litigation and who have historically filed some of the most important proposals on potentially material issues for their companies.

The 2025–2026 proxy season ultimately demonstrates both the resilience and the fragility of the shareholder proposal system. Shareholders kept raising concerns about governance, risk oversight, and corporate conduct. Some companies kept engaging constructively. But the absence of consistent regulatory oversight has introduced uncertainty, uneven outcomes, and shifted investor-company relations onto a more adversarial footing, dependent on litigation and escalatory tactics, rather than orderly SEC staff assessment of whether a proposal is consistent with the rule.

Investment Organizations Letter to Chairman Paul Atkins re Rule 14a-8 Jan 14, 2026

January 14, 2026

Dear Chairman Atkins and Mr. Moloney,

Thank you for taking the time to meet with us on December 17, 2025 to discuss ourconcerns regarding recent changes to the Division of Corporation Finance no-actionletter process for shareholder proposals and potential changes by the Commission toRule 14a-8.We appreciate the opportunity for an exchange of perspectives. However, we continue to have concerns.

Specifically, changes to the shareholder proposal process conflict with the Commission's tripartite mission of promoting capital formation, investor protection, and maintenance of fair and orderly capital markets. The ability of shareholders to vote by proxy on proposals made by their fellow shareholders has long been an integral part of the U.S. corporate governance system. We believe that this private ordering processhas helped facilitate capital formation.

In the intervening days since we met, we have seen a number of companies avail themselves of the opportunity to notify proponents of their intent to exclude proposals without the benefit of the Division of Corporation Finance staff’s substantive no-action letter review process. We believe the elimination of the no-action letter process for shareholder proposals will deprive investors of the opportunity to vote on numerous valid proposals. It will also work against the interests of many issuers who are now unable to obtain the Rule 14a-8 guidance that the Division staff have historically provided.

Moreover, the new approach seems inconsistent with Rule 14a-8(k). That provision contemplates that the shareholder proponent may respond in writing to a company’s stated intention to exclude a proposal, the Commission staff will then “consider fully” the proponent’s submission, and the staff will then issue a “response”, presumably that either agrees or disagrees with the company or the proponent.

In addition, we have continuing concerns about the approach outlined by Chairman Atkins to the Division Staff in his October 9th, 2025 speech at the John L. Weinberg Center for Corporate Governance. The right of shareholders under Delaware law to vote on precatory proposals is well-established, long-standing and highly beneficial for both shareholders and issuers. Indeed, a recent study (copy enclosed) concludes that shareholder activism “can positively influence firm value” and can “meaningfully shape long-term firm performance.” See “The Value of Being Heard” at page 40. Moreover, theproposed approach conflicts with the Commission’s longstanding position that “mostproposals that are cast as recommendations or requests that the board of directors takespecified action are proper under state law” as memorialized in Rule 14a-8’s note to paragraph (i)(1).

We urge the Division to engage in a robust effort to collect information from all concerned market participants regarding the shareholder proposal process to guide its consideration in this area. For example, in 2018 the SEC staff held a series of roundtables on the proxy process with investor, issuer and asset manager perspectives. As part of these roundtables, the staff invited interested members of the public to provide written comments that were considered as part of the Commission’s 2019proposed revisions to Rule 14a-8. We believe that a similar information gathering process would be beneficial if further changes to the shareholder proposal process are contemplated.

In the spirit of promoting dialogue and to better inform the Commission about the manybenefits that have resulted from the private ordering process of the shareholder proposal rule, we would like to share the following resources for your consideration:

Profs. Jill Fisch, Sarah Haan, Ann Lipton, and Amelia Miazad, Stockholder Proposals—Law and Policy Considerations, Harvard Law School Forum on Corporate Governance (December 9, 2025)

Letter to Chairman Atkins from various state fiscal officers (December 3, 2025)

Letter to Chairman Atkins from various investor organizations (November 5, 2025)

Letter to Chairman Atkins from the Council of Institutional Investors (December 30, 2025)

Letter to Chairman Atkins from the International Corporate Governance Network (October 12, 2025)

Shareholder Rights Group, Interfaith Center on Corporate Responsibility, and USSIF, Shareholder Proposals: An Essential Right (2025)

Letter to Chairman Atkins from the National Legal and Policy Center (December 18, 2025)

Christina Sautter, Texas Corporate Reforms Silence Retail Shareholders—By Design, Bloomberg (January 6, 2026)

Jasmijn Vandenberk, The Value of Being Heard: Board Responsiveness to Shareholder Proposals (September 11, 2025)

For additional resources on the shareholder proposal process, please see the InvestorRightsForum.com website.

Thank you for taking our concerns into consideration. As representatives of investors who have submitted or voted upon many successful shareholder proposals at the companies in which we invest, we welcome the opportunity to provide you with further information and perspectives as you evaluate the benefits of the shareholder proposal process.

Respectfully submitted,

Brandon Rees, Deputy Director of Corporations and Capital Markets, AFL-CIO

Steven M.Rothstein, Chief Program Officer, Ceres

Josh Zinner, CEO, Interfaith Center on Corporate Responsibility

Sanford Lewis, Director and General Counsel, Shareholder Rights Group

Maria Lettini, CEO, US SIF

Danielle Fugere, President and Chief Counsel, As You Sow

Legislative Developments in the Shareholder Proposal process

House

On September 18, 2024, the US House of Representatives passed H.R. 4790, the Prioritizing Economic Growth Over Woke Policies Act.110 The legislation is an umbrella bill incorporating a number of other bills that, among other things, significantly increase the ability of companies to exclude shareholder proposals from the proxy statement, including:

amending the Securities Exchange Act of 1934 to prohibit the SEC from compelling an issuer to include in the proxy statement any shareholder proposal or any discussion related to a shareholder proposal. The bill also expressly states the SEC may not preempt state regulation of proxy materials or shareholder proposals. (Section 2002)

increasing requirements for resubmission of proposals to require 10% voting support for a first-year proposal, 20% for a second year proposal and 40% for third year proposal, compared to current requirements of 5% voting support the first year, 15% for the second year and 25% for the third year. (Section 3101)

allowing companies to exclude shareholder proposals where the company already has policies, practices, or procedures that compare favorably with the guidelines of the proposal and address the proposal’s underlying concerns. (Section 3201)

allowing companies to exclude any proposal relating to environmental, social or political issues from proxy or consent solicitation material. (Section 3301)

allowing companies to exclude a shareholder proposal under Rule 14a-8(i) without regard to whether the proposal relates to a significant social policy issue. (Section 3401)

requiring the SEC to conduct a “wasteful and unnecessary” study every 5 years on shareholder proposals, proxy advisory firms, and the proxy process, covering a variety of topics, including the purported costs incurred by the shareholder proposal process and the “risk that shareholder proposals may contribute to the balkanization of the US economy over time.” (Section 3501)

providing that an institutional investor may not outsource voting decisions to any person other than an investment adviser or a broker or dealer that is registered with the Commission and has a fiduciary or best interest duty to the institutional investor. (Section 3901)

Senate

On September 23, 2024, S. 5139, the Empowering Main Street in America Act of 2024, was introduced. Among other things, the bill would allow a company to exclude a shareholder proposal from its proxy statement without regard to whether that shareholder proposal relates to a significant policy issue. (Section 305)

Shareholder Rights Group: At Boeing, Wells Fargo, Chevron - SEC Rulemaking Proposals Would Have Blocked Investor Engagement on Critical Issues

Immediate Release

January 7, 2019

The Shareholder Rights Group (SRG), a coalition of investors who exercise their right to file shareholder proposals, has written to the Securities and Exchange Commission (SEC) in opposition to proposed rule changes that would effectively undermine the ability of shareholders to continuously promote increased corporate responsibility and improved corporate governance. [Link to letter]

Currently, shareholders that own at least $2,000 in stock for one year have the right to engage an investee company on an issue of concern through procedures set forth in the SEC’s Rule 14a-8. In late 2019, the SEC proposed dramatic changes to the Rule, undermining shareholders’ rights to hold companies accountable for risk mitigation and crisis management. In addition to making it harder to file proposals by requiring larger or longer-term holdings, the rulemaking proposal would make it more difficult for shareholders to submit a proposal to a second or third vote by imposing steep voting thresholds – 25% support by the third year, and disallowing a proposal if it suffered a loss of momentum after that. The SRG letter notes that “[i]n practice sometimes 10% or 20% of investors represent the leading edge of an issue - the prescient minority, and therefore it is not wise for the management to discount the topic they are surfacing.”

The SRG’s letter highlights three case studies in which shareholders preemptively sought disclosure or oversight of certain issues that have proven to be significant concerns for those companies. Specifically, the SRG’s letter explains how the proposed rule changes, if they had been in effect at the time of shareholder engagement, would have interfered with investors’ ability to directly respond to recent corporate responsibility crises and controversial operations at Boeing, Wells Fargo, and Chevron.

Boeing: Prior to the two crashes of Boeing’s 737 Max airliners in 2018 and 2019, shareholders had encouraged better disclosure of Boeing’s notoriously aggressive lobbying policies, expenditures, and internal controls. Under the SEC’s proposed rulemaking on resubmissions, shareholder proposals on lobbying would have been barred beginning in 2017 – shortly before the 737 Max crashes. Yet, after the 737 Max crashes, shareholders supported lobbying disclosure with 32.6% of the vote in 2019. Had the proposed resubmission thresholds already been in place, shareholders would have been denied an opportunity to address this matter with the company in the wake of these catastrophic events.

Wells Fargo: Wells Fargo has suffered and continues to suffer a prolonged crisis of public, government, and consumer trust, having paid over $17.2 billion in penalties since 2000. The establishment of 3.5 million fictitious or unauthorized accounts, and improper practices in which 800,000 people were forced to take redundant auto insurance from 2012 to 2017, have punctuated an era of predatory practices. Had the SEC’s proposed resubmission thresholds been in place, shareholder proposals concerned about the ethical and business risks of predatory lending would have been excludable from 2013 to 2016. Additionally, under the SEC’s proposed threshold changes, shareholder proposals seeking an independent board chair would not have been permitted from 2013 to 2016 – a change that the company quickly enacted after its 2016 account fraud scandal. The failings of leadership, toxic corporate culture, and misdirected incentives have cost at least $24 billion in market value, despite early prescient shareholder engagement.

Chevron: In the U.S., advancement on corporate climate change mitigation initiatives has been driven to a large degree by shareholder proposals and shareholder engagement. One informative example is the progression of hydraulic fracturing and methane proposals at Chevron. Shareholder engagement from 2011-2015 had led to significant advancement of Chevron’s environmental practices and reporting; during this timeframe, shareholder support ebbed and flowed reaching highs of 40% (inspiring corporate action) and dipping to 26% before rebounding to over 30%. In 2018, approximately 45% of Chevron’s shareholders voted in favor of a shareholder proposal related to fugitive methane reduction, which again inspired a corporate response on the issue. However, had the SEC’s newly-proposed “momentum requirement” been in place, this natural variation of shareholder support would have meant that investors would not have been offered the opportunity to vote on that 2018 proposal that they resoundingly supported.

Sanford Lewis, Director of the Shareholder Rights Group explains in the letter that “[i]n our assessment, the SEC’s proposed proxy rule changes would disrupt functional working relationships between shareholder proponents, institutional investors, and proxy advisors and companies. The proposed rule changes would make the path of investor engagement steeper and more convoluted, adding unnecessary costs and red tape, and making it more difficult for investors to foster sustainability, risk management, and governance improvements at their companies. It would block the most established and effective path for improving environmental, social, and governance (ESG) disclosure and performance of the market.”

The Shareholder Rights Group urges all concerned investors to write to the SEC in opposition to the proposed rules by the February 3 comment deadline. Additional info on the proposed rule changes, including links to the proposed rules are included at InvestorRightsForum.com

The SEC is accepting comments on the proposed rules until February 3, 2020. Write to: Vanessa A. Countryman, Secretary, U.S. Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549-1090; Email to: rule-comments@sec.gov. Email or hard copy subject line should include reference to the File No. S7-23-19 (shareholder proposals) and File No. S7-22-19 (proxy advisors).

Investor Voice: SEC’s Proposed Rule Changes Muzzle Shareholders and Shield CEOs From Accountability

“The shareholder proposal rule is the bedrock of effective corporate engagement in the United States,” said Bruce Herbert, chief executive of Investor Voice. “For over 70 years, the shareholder engagement process has been a vital tool for stockowners to propose good ideas involving sustainability, profitability, and governance; to hold CEOs accountable for mismanagement; and to mitigate risk by addressing issues like climate change and human rights.”

SEATTLE – The U.S. Securities and Exchange Commission voted today to consider sweeping changes to the regulations governing the shareholder proposal process which negatively impact small investors as well as proxy advisory services. The proposed changes to Rule 14a-8 include substantially more strict and complicated thresholds for filing, significantly higher resubmission requirements, serious free speech infringements on independent third-party proxy advisory services, and onerous restrictions on an investor’s essential agency right to seek assistance.

“The shareholder proposal rule is the bedrock of effective corporate engagement in the United States,” said Bruce Herbert, chief executive of Investor Voice. “For over 70 years, the shareholder engagement process has been a vital tool for stockowners to propose good ideas involving sustainability, profitability, and governance; to hold CEOs accountable for mismanagement; and to mitigate risk by addressing issues like climate change and human rights.”

“These proposed changes were not asked for by investors,” Herbert continued, “they are the result of a concerted influence campaign backed by large industry associations. Key players were the Business Roundtable, National Association of Manufacturers, and the U.S. Chamber of Commerce – each of whom believes that responding to small investors creates an undue burden on the corporation.”

The proposed changes, Herbert said, are a solution in search of a problem. Trump appointees to the SEC, including Chair Jay Clayton and Commissioner Elad Roisman, argue that change is needed to ‘modernize’ the shareholder engagement process, asserting that the rules have not been “revised” in decades.

“However,” Herbert observed, “that argument is highly misleading because ‘revision’ is very different from ‘review’ – the fact is that the shareholder engagement rule has been reviewed many times over the decades and always found to be fresh and beneficial as it stood. Focusing on ‘revisions’ while ignoring ‘reviews’, as Clayton and Roisman purposefully do, is like asserting that someone who goes in for annual check-ups has received no medical attention whatsoever unless and until they undergo surgery.”

The two Democrats on the commission, Allison Lee and Robert Jackson, blasted the proposed changes as a power-grab by corporate CEOs. “The bottom line is that today’s proposals would shift power away from shareholders and towards management,” said Commissioner Lee.

Commissioner Jackson, meanwhile, argued that, while some minor reforms may be needed, today’s proposals “amount to swatting a gadfly with a sledgehammer.”

The Commission passed the motion to consider the proposed changes on a party-line vote of 3-2. The public will have only 60 days to submit comments to the SEC once the proposals are published in the Federal Register.

Contact: Bruce Herbert

206-522-3055 team@investorvoice.net

NY State Comptroller DiNapoli Statement on Proposed SEC Rule Changes

"The SEC's proposals are two of the most significant actions to restrict shareholder rights in the SEC’s history. There is no credible evidence to support the need for these proposals, and if adopted, they would undermine corporate accountability, entrench managements’ opposition to shareholder proposals and increase costs for investors. These proposals are contrary to the SEC's mission to protect investors and our financial markets. Along with other investors, I will continue to voice my opposition to these actions and my support for greater corporate accountability."

"The SEC's proposals are two of the most significant actions to restrict shareholder rights in the SEC’s history. There is no credible evidence to support the need for these proposals, and if adopted, they would undermine corporate accountability, entrench managements’ opposition to shareholder proposals and increase costs for investors. These proposals are contrary to the SEC's mission to protect investors and our financial markets. Along with other investors, I will continue to voice my opposition to these actions and my support for greater corporate accountability."

New York City Comptroller Scott M. Stringer on Proposed SEC Rule Changes

"The proposed U.S. Securities and Exchange Commission changes will compromise the independence of our contracted proxy advisers, impose limits on shareowner proposals and therefore further insulate corporate management from accountability to shareowners. If implemented, these actions would be a shameful gift to corporate executives at the expense of shareowners.”

"As Comptroller for the City of New York, I am the chief investment advisor and custodian of assets of the five New York City Retirement Systems (NYCRS) and a trustee of four of them. These Funds represent the retirement security of the City’s teachers, school employees, police and firefighters, and other employees. Many of our more than 700,000 members likely only participate in the capital markets through their role as pension fund beneficiaries and are the true main street investors whose interests the SEC should protect.

"The NYCRS are long-term shareowners of more than 3,000 U.S. public companies and are the fourth largest public pension system in the United States, with more than $200 billion in assets under management. Our funds have filed more than 1,000 shareowner proposals, almost certainly more than any other institutional investor in the world, with a record dating back 30 years.

"The proposed U.S. Securities and Exchange Commission changes will compromise the independence of our contracted proxy advisers, impose limits on shareowner proposals and therefore further insulate corporate management from accountability to shareowners. If implemented, these actions would be a shameful gift to corporate executives at the expense of shareowners.

"The proposed rules seek to remedy problems that do not exist but are merely false narratives put forward by corporate executives who want to limit the ability of investors to push for change and to hold them accountable for runaway CEO pay, excessive risk-taking and irresponsible and harmful business practices.

"These are mechanisms through which we and other shareowners have pushed for anti-discrimination policies, greater diversity in the C-suite, better climate policies and improved transparency and accountability in our interests as long-term investors. We should be demanding more of this, not less."

Council of Institutional Investors: Fact Sheet on Proxy Advisory Firms and Shareholder Proposals Nov. 5, 2019

Most public companies do not receive any shareholder proposals. On average, 13% of Russell 3000 companies received a shareholder proposal in a particular year between 2004 and 2017. In other words, the average Russell 3000 company can expect to receive a proposal once every 7.7 years. For companies that receive a proposal, the median number of proposals is one per year.

1. The Business Roundtable, National Association of Manufacturers and other

management groups’ claim that proxy advice is rife with errors is based on anecdote not evidence.

· The SEC comment file for the SEC’s Nov. 15, 2018, proxy roundtable includes a number of letters that assert that errors in proxy reports are endemic. But the letters offer very few examples and most of those do not identify the company and cannot be checked. CII believes most claims of errors actually are methodological differences.

· The only study that CII is aware of that purports to tote up proxy advisor errors alleges just 39 factual errors over nearly three years (or 0.1% of more than 30,000 reports by leading proxy advisory firms Institutional Shareholder Services (ISS) and Glass Lewis during that period). And the study inflates the claimed error rate. CII’s own analysis of the study found that no more than 17 of the claims of factual error had merit.

· CEO and board member dislike of proxy advisors appears driven by discomfort with the role of proxy research to be critical and raise questions. The charge of systemic factual error appears to be fabricated as a means to quash critical analysis and commentary.

2. Claims that proxy advisory firms wield excessive influence over how institutional investors vote confuse correlation with causation.

· Many pension funds and other institutional investors buy proxy and review advisors’ research and recommendations but vote according to their own guidelines and policies. According to ISS, 85% of its top 100 clients use a custom voting policy.

· It is wrong and insulting to suggest that institutional investors “robo vote”—vote in lockstep with proxy advisor recommendations. While ISS recommended voting against say-on-pay proposals at 12.3% of Russell 3000 companies in 2018, just 2.4% of those companies received less than majority shareholder support on their say-on-pay proposals. In 2019, Glass Lewis recommended in favor of 89% of directors and 84% of say-on-pay proposals, while directors received average support of 96% and say-on-pay proposals garnered average support of 93%.

· Academic research has found that while both ISS and Glass Lewis appear to have some impact on shareholder voting, media reports often substantially overstate the extent of that influence.

3. The proposed mandate that proxy advisory firms let companies review the firms’ reports before investor clients see them amounts to unprecedented interference in the free market and is the opposite of what is required by regulation of stock analyst reports.

· Current rules prohibit analysts from sharing draft research reports with target companies, other than to check facts after approval from the firm’s legal or compliance department.

· FINRA Rule 2241, which the SEC approved, establishes this safeguard to, as the SEC has explained, “help protect research analysts from influences that could impair their objectivity and independence.”

· If the SEC adopts its proxy advisor regulation, an analyst and a proxy advisor could write a report on the same company and the analyst would violate securities laws by showing it to the company in advance, while the proxy adviser would violate the law if it did not show it to the company in advance.

· This is the very definition of arbitrary and capricious government action.

4. Three SEC commissioners are attempting to jam through fundamental changes without appropriate analysis and public comment.

· The predicate for the SEC’s new, heavy-handed regulatory structure for proxy advisory firms is a significant change made by the SEC on Aug. 15, 2019, on a 3-2 vote, without any public comment, zero cost-benefit analysis and limited and flawed legal justification.

5. Shareholder proposals have proven to be a key channel for effective shareholder engagement with public companies for more than half a century.

· Shareholder proposals permit investors to express their voice collectively on issues of concern to them, without the cost and disruption of waging proxy fights.

· Shareholder proposals have encouraged many companies to adopt governance policies that today are viewed widely as best practice.

o Electing directors by majority vote, rather than by plurality, a radical idea a decade ago when shareholders pressed for it in proposals, is now the norm at 90% of large-cap U.S. companies.

o Similarly, norms such as independent directors constituting a majority of the board, independent board leadership, board diversity, sustainability reporting, non-discrimination policies and annual elections for all directors all were advocated early through shareholder proposals.

· Shareholder proposals are a critical tool for expression of the collective views of holders, permitting them to communicate with each other as well as the company on whether an issue or approach has support. Another tool is voting against directors, but the message from negative voting on directors when the concern is a specific policy or disclosure is much less focused or clear.

6. Shareholder proposals are not a significant burden to U.S. public companies.

· Shareholder proposals are almost always non-binding. The board actually does not have to do anything in response to a proposal.

· Most public companies do not receive any shareholder proposals. On average, 13% of Russell 3000 companies received a shareholder proposal in a particular year between 2004 and 2017. In other words, the average Russell 3000 company can expect to receive a proposal once every 7.7 years. For companies that receive a proposal, the median number of proposals is one per year.

· Companies exaggerate the cost of shareholder proposals. Most of the cost involves attempts by management to exclude proposals from their proxy statements, which is a choice made by management. The cost to put a proposal on the proxy ballot is de minimis.

· CEO advocacy organizations say that shareholder proposals keep private companies from doing an IPO, an unsupportable and fact-free assertion. It is ludicrous to argue that a board would forgo access to public capital markets because in the next eight years the company may face a nonbinding shareholder proposal requesting better disclosure on its carbon footprint or the annual election of all directors.

7. Additional curbs on shareholder proposals are not needed.

· Raising resubmission thresholds will stifle new ideas and issues, which typically take time to gain traction with investors.

· The raised resubmission thresholds will keep topics off corporate ballots for years, even though circumstances may change at a company (e.g., independent board leadership tends to be seen as much more urgent when a company is in crisis, and the proposed new thresholds are likely to bar a proposal to separate the roles of CEO and chair at companies with the worst governance records).

· The increased ownership thresholds will especially hamper small investors, the very market participants that SEC Chairman Jay Clayton has made it a priority to protect.

· Until 1983, ownership of a single share of stock carried the right to propose a shareholder resolution. Now we are on a slippery slope that strips that right from more and more small shareholders, whose ideas can be as important and valuable to consider as those of larger holders.

AS YOU SOW: As Shareholder Support for Climate Change and other Environmental, Social, and Governance Issues Grows, SEC Votes to Restrict Shareholder Voice

“The SEC has been unable to point to any demonstrable problem with the current shareholder system or make a case for how its proposal to limit shareholder rights will improve company value,” said Danielle Fugere, president of As You Sow. “To the contrary, this proposed rulemaking has the potential to increase shareholder and company risk, particularly regarding growing climate concerns. We don’t believe that it will withstand public or legal scrutiny.”

BERKELEY, CA—NOV. 5, 2019—The U.S. Securities and Exchange Commission (SEC), led by Chairman Clayton, voted today to severely limit the rights of shareholders, especially small shareholders to file proposals at companies. The SEC 14a8 process was created to ensure that shareholders have the right to seek transparency and disclosure from companies or raise significant policy issues that can create risk or harm company value over time. Such proposals, which are advisory and not mandatory even with 100% of the vote, have the goal of raising critical issues in front of management, boards, and company shareholders. Today’s draconian vote, split along party lines, would limit investor rights in ways that are incompatible with the basic premise that shareholders are owners of companies and should have a voice in the companies they own.

“With this vote, the SEC has apparently inverted its mandate of protecting shareholders to that of protecting companies from shareholder input — even where company action creates increasing risk to shareholders, people, or the environment,” said Andrew Behar, CEO of As You Sow. “This proposal flies in the face of the SEC’s mandate of ensuring transparency, open discussion, and company responsiveness to shareholder concerns.”

Shareholder proposals have served an important role in bringing cutting edge issues to the attention of management and boards, informing shareholders of growing risk, and increasing productive discussion of significant policy issues — in short, increasing transparency and shedding light on company actions. “Shareholders and companies have been well served by this process over the years; allowing company actions to fall back into the shadows is a giant step backward for all,” said Behar.

Climate proposals are an important example of how shareholders have successfully used the process to flag the growing risk to companies and investors of inaction on climate change. Shareholder proposals have shined a light on the importance of climate change; highlighted the risks of inaction; underscored opportunities for responsive companies; flagged lead actors and lagging companies; and ensured that the market is appropriately addressing growing systemic climate risk.

“The SEC has been unable to point to any demonstrable problem with the current shareholder system or make a case for how its proposal to limit shareholder rights will improve company value,” said Danielle Fugere, president of As You Sow. “To the contrary, this proposed rulemaking has the potential to increase shareholder and company risk, particularly regarding growing climate concerns. We don’t believe that it will withstand public or legal scrutiny.”