Shareholder Proposals and Corporate Governance in a Season of Regulatory Uncertainty

Access the full text here.

Executive Summary

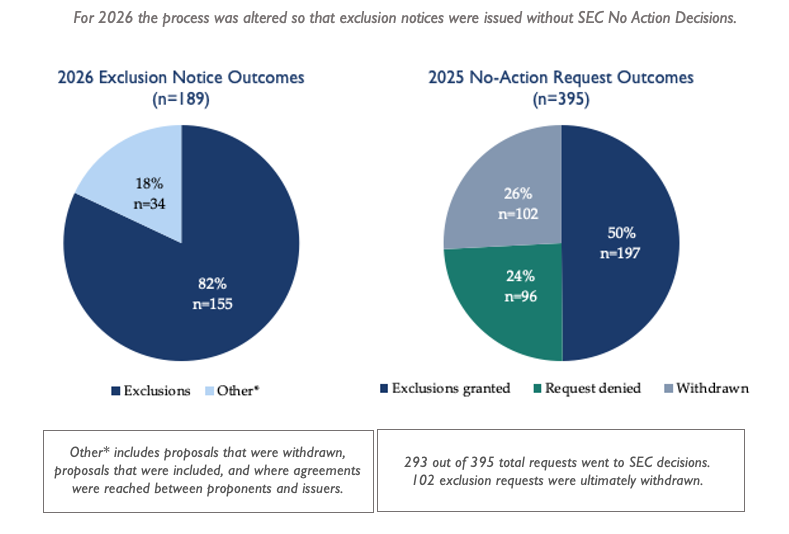

In the 2026 proxy season, the Securities and Exchange Commission (SEC) Division of Corporation Finance upended a long-standing practice of issuing informal decisions on whether shareholder proposals are excludable by the companies receiving them.

Although the SEC shareholder proposal rule, Rule 14a-8, remained in force, the SEC’s administrative dispute resolution mechanism—neutral staff review through the no-action process—was gone. The Division cited resource constraints and the sufficiency of existing guidance to justify suspending the no-action process for the current proxy season. As it stated on November 17, “due to current resource and timing considerations… as well as the extensive body of guidance from the Commission and the staff available to both companies and proponents… the Division has determined to not respond to no-action requests…” How did these changes affect the ability of shareholders to use the proposal process to raise potentially material issues with their companies and fellow shareholders? How did the SEC’s absence as a neutral arbiter of exclusion claims affect how issuers and proponents behaved? How did it affect the efficiency and effectiveness of the shareholder proposal process as a means of placing important questions before shareholders on corporate proxy statements? This analysis examines how the shareholder proposal process functioned during the 2025–2026 proxy season to identify patterns in how companies and shareholders navigated the process in the absence of routine staff review, to assess issues of fairness, balance, and efficiency and to make recommendations based on the lessons from the season.

The data indicate a chilling effect on both proponents and issuers. Shareholders filed approximately 20% fewer proposals for the 2026 season. Companies filed over 100 fewer exclusion notices.

Many companies, it seems, made a prudent judgment: without SEC staff guidance on individual proposals, unilateral exclusion carried too much risk, including proponent litigation, reputational risk, potential fuel for a proxy fight over director elections, and other concerns. Rather than exploit the absence of oversight, many companies receiving proposals let the proposals go to the proxy, sometimes even explicitly citing the lack of SEC guidance as their reason for including proposals they believed might otherwise be excludable. Other companies similarly situated engaged with proponents to produce settlement agreements.

The rate at which proposals were excluded by companies in proportion to the number of proposals filed, in the absence of the SEC’s informal determinations, was similar to the rate excluded last year after SEC determinations. Yet, analysis of these exclusions revealed several important trends.

Comparison of 2025 and 2026 Process Outcomes

One of most common justifications for excluding proposals was the ordinary business rule—a determination that typically turns on subjective factors and has historically benefited from substantive SEC staff evaluation. Unfortunately, the largest portion of these exclusions clearly disadvantaged proponents who were either filing proposals on emerging risks on which staff had not previously opined or had refined a prior proposal’s language to address prior SEC staff concerns about prescriptive language. In both categories, the absence of SEC involvement undermined an orderly process and fair resolution of disputes over excludability, allowing exclusions to proceed despite the lack of staff guidance.

This exclusion trend is particularly troubling for proposals addressing an issue on which the staff has never opined. Even if the proposal concerned a significant emerging risk, exclusion could proceed despite the lack of staff guidance.

For example, at proposal at Amazon requesting company-specific disclosure of workforce risks tied to evolving U.S. immigration policy was excluded despite the absence of prior staff guidance on the topic. Proponents sought analysis of how recent and anticipated changes to immigration rules—particularly those affecting H-1B visa holders, warehouse labor, and truck drivers—could disrupt workforce, logistics capacity, and operating costs. Given the scale of Amazon’s workforce and reliance on these labor segments, this is an issue that a reasonable investor could view as financially material and decision-useful, yet the proposal was excluded without the benefit of any staff position addressing similar subject matter.

Similarly, on a year-to-year basis, the SEC sends signals to proponents and issuers regarding whether proposal language is too prescriptive, allowing proponents to revise proposals accordingly. This iterative feedback loop aligns proposal drafting with evolving staff interpretations. However, in the 2026 proxy season, such revisions were not ratified by staff review. As a result, issuers exercised unilateral discretion, and even proposals that may have been revised in good faith to conform with prior SEC guidance were nevertheless excluded.

For example, at AbbVie Inc., shareholders requested that the board oversee human rights due diligence to produce an impact assessment identifying actual and potential adverse human rights impacts in the company’s operations and supply chain, including effects on the right to health. Notably, this proposal appears to have been drafted to be less prescriptive than a prior 2025 proposal seeking a human rights impact assessment submitted to Eli Lilly, which the staff had permitted to be excluded on micromanagement grounds. The Eli Lilly proposal explicitly mandated the assessment cover “operations, activities, business relationships, and products”. By contrast, the AbbVie proposal narrowed and generalized the request—focusing on board oversight and an impact assessment framework rather than dictating exhaustive coverage parameters. Despite this apparent effort to align with prior staff reasoning and reduce prescriptiveness, AbbVie relied on the earlier Eli Lilly determination to justify exclusion. This illustrates how, in the absence of updated staff review, even materially revised proposals that address prior deficiencies can be excluded based on inapposite precedent.

Thus, an analysis of the ordinary business exclusions reveals that exclusions during this season disproportionately blocked (i) proposals addressing emerging issues lacking precedent and (ii) proposals that had undergone compliance-oriented revisions based on prior staff signals. The absence of no-action letters was therefore not neutral—it both impeded shareholders’ ability to surface new, financially relevant risks and disrupted the established corrective process that typically refines proposal language over time.

In another significant portion of exclusions, the companies claimed that their own activities substantially implemented the proposal. SEC staff is better positioned to provide a neutral evaluation of whether the company activities go as far as a proposal requests. These determinations are not appropriately left to the issuers.

Technical grounds—such as providing inadequate documentation that the proponent owned the necessary shares, or missing filing deadlines—accounted for another meaningful portion of exclusions. Some of these deficiencies seemed clear-cut. But without a structured opportunity for proponents to respond, questions remained about whether some of these technical exclusions rested on incomplete or disputed records that SEC staff would historically have scrutinized.

The disappearance of routine administrative review also caused at least six proponents to bring their disputes into federal court. Three of these cases resolved quickly after the companies agreed to include the proposals or provide the requested disclosure. These cases underscore how, in the absence of staff intermediation, formal legal action began to substitute for what had previously been an administrative and negotiated process. As proponent driven litigation became the primary enforcement mechanism for Rule 14a-8, a structural imbalance also took shape: the ability to defend a proposal increasingly depended on having the financial and legal resources to sue, in contradiction of the rule’s share ownership thresholds—which were designed to give even modest Main Street shareholders a voice.

This shift reflects a broader reconfiguration of how the rule operates in practice. Rule 14a-8 has historically depended on a combination of administrative oversight, evolving staff interpretation, and iterative dialogue between companies and investors. When the administrative layer was removed, interpretive authority shifted to issuers, and dispute resolution migrated to litigation and market pressure.

In that environment, the dynamics between proponents and companies changed materially. Proponents—who typically seek collaborative engagement with the company and dialogue with fellow shareholders—were forced into a position where they must consider escalation, including litigation, to ensure inclusion of proposals on the proxy.

The report concludes with five key recommendations for strengthening Rule 14a-8 and the shareholder proposal framework:

Preserve Rule 14a-8. The shareholder proposal mechanism is a vital communication channel between investors and corporate management. Weakening or eliminating it would undermine shareholders’ ability to raise governance concerns and hold management accountable.

Restore the no-action process. The SEC should revive its administrative process for resolving proposal exclusion disputes. Without it, conflicts are pushed into costly federal litigation or contentious shareholder campaigns. Some streamlining is possible for clear-cut procedural defects, but contested or fact-dependent claims still require meaningful staff review.

Eliminate “no-objection” letters. The practice of issuing no objection letters based solely on a company’s own unverified representations is inconsistent with Rule 14a-8’s intent. It implies administrative endorsement of unilateral exclusions regardless of consistency with the rule, and should be discontinued.

Issue clearer, more objective guidance. While appropriately restoring clarity about ensuring that proposals are relevant to the companies receiving them, Staff Legal Bulletin 14M also introduced excessive subjectivity into key exclusion determinations—particularly on “ordinary business” and “micromanagement” grounds. The subjective criteria provide staff with too much discretion; returning to more objective standards would improve predictability and reduce the need for repeated case-by-case adjudication.

Protect smaller shareholders’ access. Any reforms should ensure the process remains accessible to individual investors and smaller asset managers, who are unlikely to pursue litigation and who have historically filed some of the most important proposals on potentially material issues for their companies.

The 2025–2026 proxy season ultimately demonstrates both the resilience and the fragility of the shareholder proposal system. Shareholders kept raising concerns about governance, risk oversight, and corporate conduct. Some companies kept engaging constructively. But the absence of consistent regulatory oversight has introduced uncertainty, uneven outcomes, and shifted investor-company relations onto a more adversarial footing, dependent on litigation and escalatory tactics, rather than orderly SEC staff assessment of whether a proposal is consistent with the rule.

Investor Representatives File Lawsuit Challenging Unlawful Restriction of Shareholder Rights

March 19th, 2026

Lawsuit Seeks to Block Change by SEC that Encourages Companies to Exclude Shareholder Proposals from Company Proxy Materials

A pair of investor representative groups dedicated to corporate responsibility and the rights of investors today filed a legal challenge to a new policy from the Securities and Exchange Commission’s (SEC) Division of Corporation Finance. The policy undermines a long-standing rule that governs shareholder proposals, which have been a linchpin for decades of productive engagement between companies and shareholders on matters related to long-term corporate value.

The Interfaith Center on Corporate Responsibility (ICCR) and As You Sow, represented by Democracy Forward, seek to stop implementation of the new policy, which gives companies an effective rubber-stamp from the SEC to stop investors from presenting and voting on proposals regarding issues directly relevant to a company’s long-term performance and risk profile.

The SEC’s revised policy allows companies to omit shareholder proposals by filing a simple letter and receiving a “No Objection” statement from the SEC, without benefit of any analysis by the SEC of the company’s claims or proponents’ response. Omitting a proposal from the company proxy prevents shareholders from making and voting on proposals that raise concerns about a company’s long-term performance and risk profile.

“The SEC’s actions in undermining the shareholder proposal process are a short-sighted departure from decades of precedent in which shareholder proposals, a critical tool in a private ordering process, have led to important improvements in corporate governance and corporate practices that benefit both companies and investors. This long-standing process has given generations of American investors greater voice and power, in turn helping build a stronger and more dynamic economy, and safeguarding the investments that millions of American families depend upon,” said ICCR CEO Josh Zinner.

“Both companies and investors benefit from the give and take provided by the shareholder proposal process,” said Danielle Fugere, President & Chief Counsel of shareholder representative As You Sow. “Eroding shareholders’ right to bring issues of concern to a vote of shareholders weakens an important check on company action and reduces information to shareholders. Since proposals are generally non-binding, the only real benefit of these changes appears to be shielding companies from having to consider hard issues that would be easier to sweep under the rug. This ultimately weakens the fundamentals of capitalism and investor confidence in the market.”

The SEC has long had an effective process, pursuant to Rule 14a-8, that generally requires companies to include shareholder proposals in a company’s proxy materials unless a company challenged the proposal. Under the prior process, SEC staff exercised its independent judgment by assessing the validity of a company’s claim that the proposal could be excluded. Proponents and companies were not formally bound by the SEC’s decision, but they almost universally respected them as conclusive. Under the new process, a company need not meet Rule 14a-8’s burden of proving that their omission of a shareholder proposal is justified. Now, the SEC accepts at face value a company’s “unqualified representation” and issues a letter stating that the SEC has “No Objection” if the company omits the resolution.

“The new SEC policy is an undemocratic hall pass to corporate mismanagement that sends a message to investors to ‘sit down and shut up’ about how the company they own is managed,” said Skye Perryman, President and CEO of Democracy Forward. “This policy is inconsistent with existing SEC rules, and was adopted without following the legally-required process to consider a policy change. We are honored to work with corporate responsibility advocates to challenge this new policy and to fight for the rights of shareholders to have a say in how their investments are managed.”

The case is ICCR et al. v. SEC et al. in the U.S. District Court for the District of Columbia. The legal team at Democracy Forward on this case includes Simon Brewer, Brian Netter, and Victoria Nugent.

Read the complaint here. Access the full article here.

Democracy Forward Foundation is a national legal organization that advances democracy and social progress through litigation, policy, public education, and regulatory engagement. For more information, please visit www.democracyforward.org.

US SIF’s 30th Anniversary “Trends Report”

US SIF’s latest “Trends Report” Finds Sustainable Investing Asset Base Holding Amid Political Headwinds

Sustainable assets account for 11% of total market AUM; climate and client customization drive activity, while themes like artificial intelligence (AI), biodiversity, and Indigenous People’s rights gather steam.

Highlights

US SIF analysis records the US market size as $61.7 trillion, of which $6.6 trillion (versus $6.5 trillion in 2024) were identified or marketed as sustainable or ESG investments.

53% of individuals expect the sustainable investment market to grow over the next year, compared to 73% in 2024.

Political pushback has moderated, not reversed, ESG activity with nearly half (46%) reporting no impact to how their organization approached sustainability, while 29% said they now focus explicitly on demonstrable financial materiality; one in four have stopped using the ESG acronym.

Investors are currently prioritizing the areas of the economy with high emissions and investing in the transition including energy, innovation, and transport (with 86%, 76% and 72% invested respectively).

When it comes to strategies, ESG integration remains the mainstream default with 77% using this approach.

Looking ahead, impact investing showed the strongest growth runway with 46% saying they expect their organization to increase its impact investing activities over the next three years, followed by sustainability-themed investing (43%) and ESG integration (38%).

Washington D.C., December 9, 2025 – On its 30th anniversary, the US SIF Foundation’s flagship report, US Sustainable Investing Trends 2025/2026, takes the pulse of the US sustainable investing market and finds that assets have remained steady, even amid political pushback.

Using Securities and Exchange Commission filings, US SIF places the overall US market size at $61.7 trillion, with $6.6 trillion marketed specifically as “sustainable” or “environmental, social and governance” (ESG) investments – a modest increase from $6.5 trillion in 2024, reflecting stable investor commitment. Sustainable assets represent 11% of the overall market size, versus 12% last year, a marginal decline likely due to the increase in the overall value of the market in 2024.

Sixty-nine percent of the US market AUM, or $42.7 trillion, was covered by an active stewardship policy.

Launched in 1995, the Trends report has provided the foundational data needed to understand the evolving sustainable investing market for three decades. In partnership with SDGlabs.ai, US SIF reviewed SEC disclosure Forms ADV and 13F, public websites and reporting, and 270 survey responses to create the definitive baseline of the US sustainable investment market.

Political Impact on Sustainable Investing Activity

The evolving dynamics of US politics are shaping investor sentiment and approaches to sustainability in noticeable, if uneven, ways. Rather than a wholesale pullback, the current moment is characterized by adjustment: investors are holding to their sustainability commitments while recalibrating terminology, stewardship practices, and disclosure framing to fit shifting legal and political conditions.

When asked whether certain events or issues affected their decision to increase sustainable investments in 2025 and beyond, 62% said the political environment had no effect on their decision, while 22% said they would increase investments.

“What we’re witnessing is that there has not been a retreat from sustainable investing. Over three decades, we’ve seen this industry evolve from a niche concept to mainstream investment approach. The shifts we’re seeing reflect a pragmatic adaptation to the current environment while maintaining focus on the long-term drivers of value and changing market risks and opportunities.”

Maria Lettini, CEO of US SIF

Climate change (52%), client-driven customized investing (41%), and severity and frequency of catastrophic climate events (38%) were the top issues driving an increase in sustainable investment activities. Loss of biodiversity (34%) and food insecurity (24%) rounded out the top five.

Notably, 23% of respondents indicated that AI was positively affecting their decision on whether to increase sustainable investments in 2025 and beyond. Heightened attention to Indigenous Peoples’ rights (with 16% increasing and 81% maintaining activity) and migration (11% increasing and 87% maintaining) underscores growing focus on social issues at the nexus of major sectoral trends in the extractive industries, the energy transition, infrastructure, and related sectors.

Industry Comments

"The continued strength in sustainable investing AUM demonstrates that ESG integration has become a fundamental part of investment strategy, not a passing trend. At G&A, we've tracked thousands of companies increasingly adopting sustainability reporting and disclosure practices in response to investor demand. This alignment between investor capital allocation and corporate transparency is strengthening markets, improving corporate resilience, and creating long-term value for all stakeholders and the broader economy.”

Louis Coppola, CEO & Co-Founder, G&A Institute

“That this report found that 69% of the entire US market is covered under a stewardship policy underscores the importance of this approach in driving value. Whether through proxy voting, direct engagement or other stewardship strategies, global companies can expect to hear from the investment community about issues that affect corporate resilience.”

Lisa Hayles, Director of Sustainability and Stakeholder Engagement, Trillium Asset Management

“At a time when the broad expectation was that sustainable investing assets would contract, this year’s Trends report shows that the industry is staying the course and committed to providing long-term value. This aligns with Calvert’s time-tested responsible investment philosophy.”

Anthony Eames, Managing Director, Responsible Investment Strategy, Calvert Research and Management

“The 2025/2026 Trends report underscores that investors remain focused on material sustainability risks and opportunities that affect business resilience and promote value creation over the long term. While approaches to these issues continue to evolve, enhanced corporate disclosure remains essential for investors to mitigate risks and capitalize on opportunities, such as those presented by climate change and emerging artificial intelligence (AI) technologies.”

Amy D. Augustine, Director of ESG Investing, Boston Trust Walden

Access the full report, here.

ICGN Letter to SEC on Shareholder Proposals

Letter from Jen Sisson, CEO of ICGN on 10th December 2025

Dear Chairman Atkins, and Commissioners Uyeda, Peirce and Crenshaw,

Subject: Comments on the SEC Statement on Rule 14a-8 - No-Action Requests

The International Corporate Governance Network (ICGN) would like to offer its perspective on the SEC Division of Corporation Finance statement, published on November 17, 2025, regarding no-action requests under Rule 14a-8.

Led by investors responsible for assets under management of over US$90 trillion, ICGN promotes high standards of corporate governance globally. Our members – both asset owners and asset managers – have significant exposure to the U.S. market.

We are deeply concerned by the Division of Corporation Finance’s announcement that it will not substantively respond to most Rule 14a-8 no-action requests for the 2025–2026 proxy season. We are concerned that the narrowing of shareholder proposal rights appears part of a broader shift that reduces the avenues through which investors can engage with portfolio companies, compounded by recent changes to interpretations of Section 13D and 13G. Taken together, these developments risk adding tensions between company owners and management, and diminish investor confidence in U.S. corporate governance standards and thereby weaken the appeal of U.S. capital markets globally.

Why shareholder resolutions are an important mechanism

Shareholder resolutions are a vital mechanism for company owners to surface ideas and raise concerns with company management and all shareholders. They have been a key driver of corporate governance improvements in the United States. For example, shareholder resolutions have been successful in promoting annual director elections and establishing simple majority vote requirements. Shareholder proposals helped these good governance practices to become norms, based on a market-led approach, without regulation or standards. Hundreds of constructive dialogues, resulting in increased corporate transparency and improved governance, have been facilitated by shareholder resolutions at minimal cost to issuers and investors.

Each investor has their own approach to decide how to vote on a shareholder resolution. Across the market, resolutions that obtain significant shareholder support tend to be those that are not overly prescriptive for company management and that concern issues investors deem financially material for the success of the company. Shareholders tend to support proposals that can catalyse improvements in governance, reporting, risk management, and long-term strategic thinking. Academic research shows that governance provisions restricting shareholder rights, such as limits on the ability to propose resolutions, are associated with lower firm valuation and weaker stock performance.

Shareholder resolutions can help provide accountability when other mechanisms fail. They also signal investor sentiment to the company. High support levels for a proposal can drive rapid governance improvements, but even modest levels of support can prompt constructive engagement between boards and investors.

Why the SEC No Action Process should be protected

ICGN believes that the ability to file shareholder proposals is a fundamental ownership right.

For decades, issuers and investors have relied on SEC staff guidance, and although purely advisory, it has served as an independent, impartial, trustworthy check that provided procedural clarity and curbed potentially arbitrary exclusion of shareholder proposals by boards of directors.

According to the Statement, a company will be able to obtain an SEC ‘no-objection’ based solely on the company’s unqualified representation that it has a reasonable basis to exclude the proposal based on the provisions of Rule 14a-8, SEC guidance and/or judicial decisions. Without conducting an evaluation of the adequacy of the representation, the SEC’s staff will not object to the company omitting the proposal from the ballot.

By stepping back from the process, the SEC risks significantly diminishing shareholder voice and reducing important checks and balances that exist to protect the long-term interest of the company and its owners. Without the traditional buffer of a staff no-action determination, boards of directors may face increased opposition from investors concerned that relevant shareholder proposals may have been omitted without a valid reason. Furthermore, without SEC staff guidance, companies may be exposed to increased litigation, as proponents of shareholder resolutions that have been omitted by companies may seek judicial clarification in the absence of SEC staff assessment.

We regret to hear that the SEC intends to withdraw from substantive 14a-8 review. Rule 14a- 8 has facilitated a critically important private ordering process - but private ordering only works with regulatory oversight.

A call for the SEC to reconsider its Statement and launch a public consultation

ICGN recognises the resource pressures the Division faces, but the shareholder proposal process plays a vital role in surfacing material risks and enabling constructive investor- company dialogue. We believe that the existing process is well understood and has been supportive of well-functioning markets, and therefore we strongly support the SEC No Action Process being protected.

The Division’s independent review has historically provided transparency, predictability and a neutral reference point for both companies and investors. Removing or significantly narrowing that role risks eroding investor voice, imposing disproportionate burdens on minority and smaller proponents, and increasing costly litigation. As we believe this is not in the interest of efficient and fair capital markets, we respectfully ask that the SEC reconsider its statement.

We are concerned that this shift is occurring through staff announcements and public remarks, rather than through the formal rulemaking process. As highlighted in our 20 October letter, we encourage the Commission to consider returning to public consultation processes on matters that substantively alter policy, following a formal notice-and-comment process under the Administrative Procedure Act. We believe that the absence of public consultations on important announcements which may negatively affect shareholder rights, risks lowering the quality of the highly regarded due process and governance standards in the United States, thereby presenting a risk to the attractiveness of U.S. capital markets and impact the valuation of U.S. companies by investors.

We would welcome the opportunity for further dialogue on these issues. Should you have any question, please contact Severine Neervoort, Global Policy Director at policy@icgn.org.

To learn more, please visit ICGN’s Website.

Legislative Developments in the Shareholder Proposal process

House

On September 18, 2024, the US House of Representatives passed H.R. 4790, the Prioritizing Economic Growth Over Woke Policies Act.110 The legislation is an umbrella bill incorporating a number of other bills that, among other things, significantly increase the ability of companies to exclude shareholder proposals from the proxy statement, including:

amending the Securities Exchange Act of 1934 to prohibit the SEC from compelling an issuer to include in the proxy statement any shareholder proposal or any discussion related to a shareholder proposal. The bill also expressly states the SEC may not preempt state regulation of proxy materials or shareholder proposals. (Section 2002)

increasing requirements for resubmission of proposals to require 10% voting support for a first-year proposal, 20% for a second year proposal and 40% for third year proposal, compared to current requirements of 5% voting support the first year, 15% for the second year and 25% for the third year. (Section 3101)

allowing companies to exclude shareholder proposals where the company already has policies, practices, or procedures that compare favorably with the guidelines of the proposal and address the proposal’s underlying concerns. (Section 3201)

allowing companies to exclude any proposal relating to environmental, social or political issues from proxy or consent solicitation material. (Section 3301)

allowing companies to exclude a shareholder proposal under Rule 14a-8(i) without regard to whether the proposal relates to a significant social policy issue. (Section 3401)

requiring the SEC to conduct a “wasteful and unnecessary” study every 5 years on shareholder proposals, proxy advisory firms, and the proxy process, covering a variety of topics, including the purported costs incurred by the shareholder proposal process and the “risk that shareholder proposals may contribute to the balkanization of the US economy over time.” (Section 3501)

providing that an institutional investor may not outsource voting decisions to any person other than an investment adviser or a broker or dealer that is registered with the Commission and has a fiduciary or best interest duty to the institutional investor. (Section 3901)

Senate

On September 23, 2024, S. 5139, the Empowering Main Street in America Act of 2024, was introduced. Among other things, the bill would allow a company to exclude a shareholder proposal from its proxy statement without regard to whether that shareholder proposal relates to a significant policy issue. (Section 305)

Shareholder Proposals and the Freedom to Invest

Investors’ right to file shareholder proposals has contributed to the success of the US capital markets.

Large, publicly traded companies play a dominant role in the U.S. economy: pharmaceutical companies influence the medicines available in our pharmacies and their cost, health insurers influence which treatments will be affordable to patients, and tech companies influence the degree to which consumers are subject to surveillance or privacy in their use of email and social media.

The free market, and the relationship between investors and issuers, is grounded in investors’ rights as company owners to elect directors as well as file shareholder proposals. The job of boards is to oversee the executives who are day-to-day managing the company. The rights to vote upon directors, as well as to present focused issues through shareholder proposals, are part of the bundle of rights investors possess and value as company owners. The unfettered exercise of these rights reinforces the relationship of trust needed for capitalism to thrive.

Shareholder proposals address issues relevant to companies that are neither trivial nor “picayune.” Risks of potential lawsuits against the company, operational disruptions from droughts, floods and fires, and of ethical scandals that shake consumer or investor confidence— these are typical issues in shareholder proposals and raise material concerns for investors. This private ordering process can allow good ideas to proliferate in the market, advancing best practices and reducing the pressure for government regulation or for more confrontational or costly approaches by shareholders, such as voting against the board, or litigation.

Without the right to make proposals, corporate management can more easily ignore the voice of small shareholders, pension funds, and other investors.

The shareholder’s right to place proposals on the proxy, and the freedom to express a collective voice by voting on such proposals, are part of the social and legal compact between investors and companies that maintains the trust needed for capitalism to thrive. This trust has resulted in the US becoming the largest and most envied capital market in the world.

Shareholder proposals are largely non-binding. Non-binding proposals give companies the flexibility to address shareholder concerns without displacing the traditional role of the board of directors to oversee the operations of the company.

What is a Shareholder Proposal?

Shareholders—as owners of a company—have a legal right to offer proposals to appear on the corporate proxy statement to be voted upon at a company’s annual shareholders meeting. Corporations are required to hold these annual meetings in order for shareholders to vote

on matters related to the corporation such as auditor ratification, election of directors, and executive compensation. The Securities and Exchange Commission (SEC) requires public companies to file an announcement ahead of the annual meeting including its items of business called the proxy statement.4 SEC Rule 14a-8 allows shareholders to submit statements of up to 500 words (“shareholder proposals”) to be included in the company’s proxy statement.

The proxy statement is therefore the vehicle by which investors are informed of proposals by other investors. SEC Rule 14a-8 defines a shareholder proposal as a specific request from the shareholder - a “recommendation or requirement that the company and/or its board of directors take action, which you intend to present at a meeting of the company’s shareholders.” The SEC states that the proposal “should state as clearly as possible the course of action” that the shareholder believes the company should follow.

“Shareholder proposals are a crucial tool for investors to engage with their companies. Engagement covers a host of strategies investors use to obtain additional information and influence the policies and practices of their portfolio companies on governance and sustainable value creation.”

Some shareholder proposals seek changes in governance infrastructure, for example, requesting that the CEO and the board chair be separate people to increase the independence of the board and its ability to oversee the company on behalf of shareholders. Or they might request a change in voting standards to allow proposals to be passed by a vote of a simple majority rather than a larger voting threshold of supermajority, thus creating a better balance of power between the company and its investors. Other proposals may address environmental or social challenges facing the company—issues that may also be the subject of a wider social or political debate, but which nonetheless have a potential financial impact on the company or the larger economy on which returns depend.

For example, a proposal may request the disclosure of the company’s assessment of its operations, policies and practices designed to mitigate environmental, regulatory or liability risks associated with its mining operations. In another instance, a proposal may request

that a company report as to its timeline and plan for how it expects to transition to meet its stated objective of net zero greenhouse gas emissions. Some of these proposals might be described as “social or political proposals,” but they must nonetheless be relevant to the company’s business according to SEC rules and comply with more than a dozen strict SEC rules for acceptable proposals and filings.

Most shareholder proposals are non-binding. Non-binding proposals give companies the flexibility to address shareholder concerns without displacing the traditional role of the board of directors to oversee the operations of the company.

Introduction to the Ordinary Business Rule

Ordinary business

A basic principle of SEC Rule 14a-8 is that a proposal should not supplant or attempt to control the day-to-day decision-making of the corporation, referred to as “ordinary business.” The company’s officers are hired to manage the company under the oversight of the board of directors. The board is accountable as an elected representative of the shareholders. As such, the management and board have important day to day discretion in running the company—who to hire, how much to pay them, what kind of products or services the corporation should offer and many other ordinary business matters that it takes to run a business.

While a focus on ordinary business is not appropriate for a shareholder proposal, the courts and the SEC have made a notable exception when shareholder proposals address important policy issues for a company on which it is appropriate for shareholders to weigh in, often referred to as the “social policy” exception. Such proposals are described as transcending ordinary business.

For instance, while the day-to-day lending practices of a bank are ordinary business, when there is evidence that the bank is engaging in predatory policies and practices, shareholders are able to file a proposal asking the company to disclose more about this issue and its current policies. Similarly, policies regarding the amount of compensation paid to employees are generally ordinary business, but proposals coming from shareholders that challenge excessive compensation of the CEO or of directors are appropriate. A pharmaceutical company’s prices for its products are ordinary business, but company policies exploiting a pandemic to exploit vulnerable consumers may be seen to transcend ordinary business. Day to day legal compliance on environmental regulations is ordinary business, but significant pollution incidents or catastrophes that a company may be liable for may be an appropriate topic for a shareholder proposal because it transcends ordinary business.

An important related limitation is for proposals not to micromanage. Even if the topic transcends ordinary business, proponents must not be so granular in their request to the company that they attempt to micromanage the business. The discretion of the board and management is protected in this process. That is why many proposals often ask the board or management to disclose more about their policies and practices, and proposals seeking action are typically advisory rather than a mandatory order.

The History of SEC rules and Shareholder Proposal Regulation

During the United States’ first century, corporations had small numbers of investors and were largely controlled by shareholders through deliberations and voting that took place at in-person shareholder meetings. As the US economy grew, and corporations had to bring in large amounts of capital from thousands of investors, shareholder meetings went from in-person affairs to being conducted by proxy, and management solicited blanket voting authority based on little or no information. Ownership and control were largely divorced, and corporate abuse of the proxy, which frustrated the free exercise of the voting rights of stockholders, was rampant. Section 14 of the Securities Exchange Act of 1934 addressed this concern by authorizing the SEC to regulate proxy solicitation.

The SEC adopted the predecessor to SEC Rule 14a-8 in 1942, recognizing that shareholders need notice of proposals to be made by fellow shareholders. One court explained that, “the rationale underlying this development was the Commission’s belief that the corporate practice of circulating proxy materials which failed to refer to the fact that a shareholder intended to present a proposal at the annual meeting rendered the solicitation inherently misleading.” SEC Staff reiterated this purpose, explaining that “[t]he Senate Banking and Currency Committee recognized the need to provide not only for disclosure of matters management planned to present, but also for shareholders to be given ‘reasonable opportunity to present their own proposals and views to fellow security holders.”

Thus, SEC Rule 14a-8 advances the overall Securities Exchange Act’s goal of shareholder democracy—a central purpose of the 1934 Act in reaction to weakening shareholder control and increasingly concentrated corporate power in professional managers. Shareholder democracy stands for the principle that, in return for access to the securities exchanges, the law provides that corporations would incur a corresponding duty to give the shareholders fair suffrage. Referring to 14a-8, one recent judicial decision noted that “[t]he Commission enshrined this edict in its regulations, believing that “fair corporate suffrage” required that all shareholders receive notice of such matters when their proxies are solicited.”

Governance Proposals

Governance proposals and the role of individual investors

Governance engagements seek to ensure that a well-functioning board can effectively oversee the interests of shareholders. For example, proposals to increase the independence of the audit or risk committee have the potential to reduce accounting fraud risk. Likewise, engagements to increase the holding period of equity-based pay reduce management incentives to manipulate short-term earnings.

Governance shareholder proposals can also increase investors’ ability to engage with companies. It has been shown that it is more costly for investors to engage with companies with entrenched managers.14 The entrenchment of management is principally measured and affected by the corporate governance infrastructure including whether the company has characteristics such as:

Staggered boards

Limits to shareholder by-law amendments

Supermajority requirements for mergers

Supermajority requirements for charter amendments

Poison pills

Golden parachutes

Shareholder proposals that improve corporate governance structures on these aspects are frequently part of an overall strategy by investors to provide a better balance of power between investors and a company’s management and board.