Governance Proposals Dominate the 2026 Proxy Season

These are highlights from an article posted by ISS-Corporate analyzing the 2026 season.

Shareholder Proposal Volume Falls to a Five-Year Low

Against these backdrops, the overall volume of shareholder proposals submitted and advanced to a vote has declined to a five-year low.

While the overall volume of proposal submissions and those appearing on the final ballot declined, governance-related proposals recorded an increase in overall volume. This relative resilience highlights the continued prioritization of core shareholder rights and board accountability mechanisms among investors as well as changes in proponents’ tactics.

In contrast, environmental and social proposals extended their downward trajectory with further declines in both the number of proposals submitted and proposals voted, reflecting a more selective investor approach toward these topics. Anti-ESG proposals, which had been rapidly increasing in volume, saw a decline as well, though they continue to comprise a meaningful portion of overall proposal volume.

The shift in proposal activity likely reflects a combination of factors, including the evolving political and regulatory landscape, the mixed success many environmental and social proposals have achieved in recent years, and the impacts of recent SEC actions.

Changes to the SEC’s shareholder proposal framework and no-action process appear to have altered the calculus for proponents, potentially discouraging some submissions while incentivizing others to pursue a more focused strategy. As a result, some proponents appear to have reduced proposal activity altogether, while others have become more selective in targeting issues and companies, or have redirected their efforts toward governance-related topics that historically receive broader shareholder support and face fewer ideological headwinds.

Taken together, these developments suggest that rather than signaling a diminished interest in environmental and social issues, the decline in proposal volume may reflect a strategic recalibration by proponents seeking to maximize impact and improve the likelihood of gaining meaningful shareholder backing.

ISS-Corporate’s Approach to Proxy Season Insight

The 2026 proxy season highlights significant changes in shareholder proposal activity. While overall proposal volume declined, governance-focused proposals remained resilient and continued to receive the strongest investor support, highlighting sustained shareholder focus on board accountability and shareholder rights. Meanwhile, environmental and social proponents appear to be recalibrating their tactics, adopting a more targeted approach.

As the 2026 proxy season concludes, these trends offer important signals about evolving investor priorities and the issues most likely to shape shareholder engagement and voting decisions in the years ahead. ISS-Corporate’s Compensation & Governance Advisory team helps companies analyze shareholder proposal trends, benchmark governance practices against market expectations, assess potential areas of shareholder concern, and develop engagement and disclosure strategies that align with investor priorities. Through data-driven insights and practical governance guidance, we support boards and management teams in preparing for future proxy seasons and strengthening shareholder relationships in an increasingly dynamic governance landscape.

Shareholder Proposals and Corporate Governance in a Season of Regulatory Uncertainty

Access the full text here.

Executive Summary

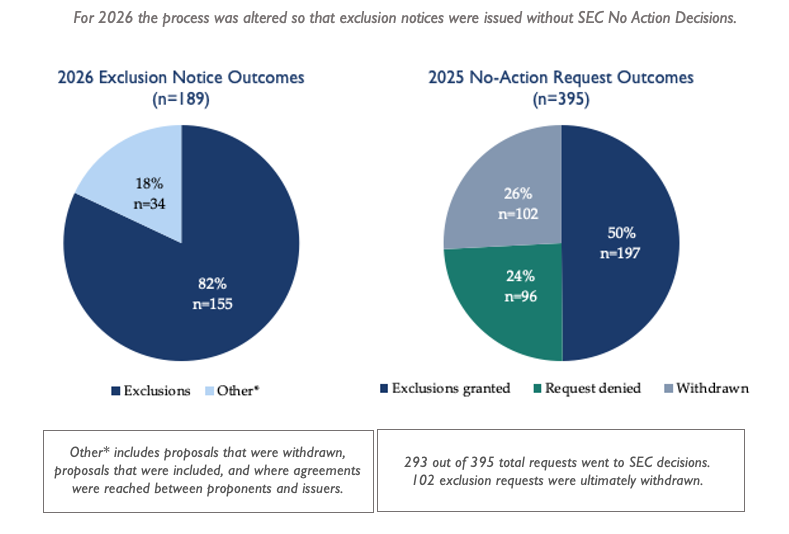

In the 2026 proxy season, the Securities and Exchange Commission (SEC) Division of Corporation Finance upended a long-standing practice of issuing informal decisions on whether shareholder proposals are excludable by the companies receiving them.

Although the SEC shareholder proposal rule, Rule 14a-8, remained in force, the SEC’s administrative dispute resolution mechanism—neutral staff review through the no-action process—was gone. The Division cited resource constraints and the sufficiency of existing guidance to justify suspending the no-action process for the current proxy season. As it stated on November 17, “due to current resource and timing considerations… as well as the extensive body of guidance from the Commission and the staff available to both companies and proponents… the Division has determined to not respond to no-action requests…” How did these changes affect the ability of shareholders to use the proposal process to raise potentially material issues with their companies and fellow shareholders? How did the SEC’s absence as a neutral arbiter of exclusion claims affect how issuers and proponents behaved? How did it affect the efficiency and effectiveness of the shareholder proposal process as a means of placing important questions before shareholders on corporate proxy statements? This analysis examines how the shareholder proposal process functioned during the 2025–2026 proxy season to identify patterns in how companies and shareholders navigated the process in the absence of routine staff review, to assess issues of fairness, balance, and efficiency and to make recommendations based on the lessons from the season.

The data indicate a chilling effect on both proponents and issuers. Shareholders filed approximately 20% fewer proposals for the 2026 season. Companies filed over 100 fewer exclusion notices.

Many companies, it seems, made a prudent judgment: without SEC staff guidance on individual proposals, unilateral exclusion carried too much risk, including proponent litigation, reputational risk, potential fuel for a proxy fight over director elections, and other concerns. Rather than exploit the absence of oversight, many companies receiving proposals let the proposals go to the proxy, sometimes even explicitly citing the lack of SEC guidance as their reason for including proposals they believed might otherwise be excludable. Other companies similarly situated engaged with proponents to produce settlement agreements.

The rate at which proposals were excluded by companies in proportion to the number of proposals filed, in the absence of the SEC’s informal determinations, was similar to the rate excluded last year after SEC determinations. Yet, analysis of these exclusions revealed several important trends.

Comparison of 2025 and 2026 Process Outcomes

One of most common justifications for excluding proposals was the ordinary business rule—a determination that typically turns on subjective factors and has historically benefited from substantive SEC staff evaluation. Unfortunately, the largest portion of these exclusions clearly disadvantaged proponents who were either filing proposals on emerging risks on which staff had not previously opined or had refined a prior proposal’s language to address prior SEC staff concerns about prescriptive language. In both categories, the absence of SEC involvement undermined an orderly process and fair resolution of disputes over excludability, allowing exclusions to proceed despite the lack of staff guidance.

This exclusion trend is particularly troubling for proposals addressing an issue on which the staff has never opined. Even if the proposal concerned a significant emerging risk, exclusion could proceed despite the lack of staff guidance.

For example, at proposal at Amazon requesting company-specific disclosure of workforce risks tied to evolving U.S. immigration policy was excluded despite the absence of prior staff guidance on the topic. Proponents sought analysis of how recent and anticipated changes to immigration rules—particularly those affecting H-1B visa holders, warehouse labor, and truck drivers—could disrupt workforce, logistics capacity, and operating costs. Given the scale of Amazon’s workforce and reliance on these labor segments, this is an issue that a reasonable investor could view as financially material and decision-useful, yet the proposal was excluded without the benefit of any staff position addressing similar subject matter.

Similarly, on a year-to-year basis, the SEC sends signals to proponents and issuers regarding whether proposal language is too prescriptive, allowing proponents to revise proposals accordingly. This iterative feedback loop aligns proposal drafting with evolving staff interpretations. However, in the 2026 proxy season, such revisions were not ratified by staff review. As a result, issuers exercised unilateral discretion, and even proposals that may have been revised in good faith to conform with prior SEC guidance were nevertheless excluded.

For example, at AbbVie Inc., shareholders requested that the board oversee human rights due diligence to produce an impact assessment identifying actual and potential adverse human rights impacts in the company’s operations and supply chain, including effects on the right to health. Notably, this proposal appears to have been drafted to be less prescriptive than a prior 2025 proposal seeking a human rights impact assessment submitted to Eli Lilly, which the staff had permitted to be excluded on micromanagement grounds. The Eli Lilly proposal explicitly mandated the assessment cover “operations, activities, business relationships, and products”. By contrast, the AbbVie proposal narrowed and generalized the request—focusing on board oversight and an impact assessment framework rather than dictating exhaustive coverage parameters. Despite this apparent effort to align with prior staff reasoning and reduce prescriptiveness, AbbVie relied on the earlier Eli Lilly determination to justify exclusion. This illustrates how, in the absence of updated staff review, even materially revised proposals that address prior deficiencies can be excluded based on inapposite precedent.

Thus, an analysis of the ordinary business exclusions reveals that exclusions during this season disproportionately blocked (i) proposals addressing emerging issues lacking precedent and (ii) proposals that had undergone compliance-oriented revisions based on prior staff signals. The absence of no-action letters was therefore not neutral—it both impeded shareholders’ ability to surface new, financially relevant risks and disrupted the established corrective process that typically refines proposal language over time.

In another significant portion of exclusions, the companies claimed that their own activities substantially implemented the proposal. SEC staff is better positioned to provide a neutral evaluation of whether the company activities go as far as a proposal requests. These determinations are not appropriately left to the issuers.

Technical grounds—such as providing inadequate documentation that the proponent owned the necessary shares, or missing filing deadlines—accounted for another meaningful portion of exclusions. Some of these deficiencies seemed clear-cut. But without a structured opportunity for proponents to respond, questions remained about whether some of these technical exclusions rested on incomplete or disputed records that SEC staff would historically have scrutinized.

The disappearance of routine administrative review also caused at least six proponents to bring their disputes into federal court. Three of these cases resolved quickly after the companies agreed to include the proposals or provide the requested disclosure. These cases underscore how, in the absence of staff intermediation, formal legal action began to substitute for what had previously been an administrative and negotiated process. As proponent driven litigation became the primary enforcement mechanism for Rule 14a-8, a structural imbalance also took shape: the ability to defend a proposal increasingly depended on having the financial and legal resources to sue, in contradiction of the rule’s share ownership thresholds—which were designed to give even modest Main Street shareholders a voice.

This shift reflects a broader reconfiguration of how the rule operates in practice. Rule 14a-8 has historically depended on a combination of administrative oversight, evolving staff interpretation, and iterative dialogue between companies and investors. When the administrative layer was removed, interpretive authority shifted to issuers, and dispute resolution migrated to litigation and market pressure.

In that environment, the dynamics between proponents and companies changed materially. Proponents—who typically seek collaborative engagement with the company and dialogue with fellow shareholders—were forced into a position where they must consider escalation, including litigation, to ensure inclusion of proposals on the proxy.

The report concludes with five key recommendations for strengthening Rule 14a-8 and the shareholder proposal framework:

Preserve Rule 14a-8. The shareholder proposal mechanism is a vital communication channel between investors and corporate management. Weakening or eliminating it would undermine shareholders’ ability to raise governance concerns and hold management accountable.

Restore the no-action process. The SEC should revive its administrative process for resolving proposal exclusion disputes. Without it, conflicts are pushed into costly federal litigation or contentious shareholder campaigns. Some streamlining is possible for clear-cut procedural defects, but contested or fact-dependent claims still require meaningful staff review.

Eliminate “no-objection” letters. The practice of issuing no objection letters based solely on a company’s own unverified representations is inconsistent with Rule 14a-8’s intent. It implies administrative endorsement of unilateral exclusions regardless of consistency with the rule, and should be discontinued.

Issue clearer, more objective guidance. While appropriately restoring clarity about ensuring that proposals are relevant to the companies receiving them, Staff Legal Bulletin 14M also introduced excessive subjectivity into key exclusion determinations—particularly on “ordinary business” and “micromanagement” grounds. The subjective criteria provide staff with too much discretion; returning to more objective standards would improve predictability and reduce the need for repeated case-by-case adjudication.

Protect smaller shareholders’ access. Any reforms should ensure the process remains accessible to individual investors and smaller asset managers, who are unlikely to pursue litigation and who have historically filed some of the most important proposals on potentially material issues for their companies.

The 2025–2026 proxy season ultimately demonstrates both the resilience and the fragility of the shareholder proposal system. Shareholders kept raising concerns about governance, risk oversight, and corporate conduct. Some companies kept engaging constructively. But the absence of consistent regulatory oversight has introduced uncertainty, uneven outcomes, and shifted investor-company relations onto a more adversarial footing, dependent on litigation and escalatory tactics, rather than orderly SEC staff assessment of whether a proposal is consistent with the rule.

The Value of Being Heard: Board Responsiveness to Shareholder Proposals

While prior research has primarily focused on the short-term market reactions to shareholder proposals and examined their outcomes in isolation, this study adopts a broader perspective by investigating how different levels of proposal responsiveness relate to firm value. We posit that the value effects of shareholder proposals are more pronounced when firms are open to dialogue with shareholders, whether publicly or privately. Using a sample of 9,764 shareholder proposals submitted to S&P 1500 firms between 2005 and 2021, we find that both voted and withdrawn proposals are similarly associated with higher firm value (measured by Tobin's Q) compared to omitted proposals. In the longer term, our results provide modest evidence that the positive effect persists primarily for withdrawn proposals, suggesting that the highest degree of responsiveness yields the greatest value creation. Furthermore, responsiveness appears to be more value-enhancing when proposals are submitted by multiple shareholders or in firms with CEO duality, indicating that both collective shareholder action and CEO power dynamics play a role. These findings imply that regulators, companies and shareholders should recognize that the shareholder proposal process can enhance firm value under certain conditions.

Read full paper

The Impact of Coordinated E&S Engagements

Authors: Elroy Dimson, Oğuzhan Karakaş, and Xi Li

As the focus on environmental and social (E&S) factors grows, shareholder organizations encourage investee businesses to act responsibly. This research studies the impact of coordinated, international E&S engagements. It shows that shareholder coalitions with clear leadership are more likely to achieve success and to deliver financial benefits to target and investor firms.

SUMMARY OF FINDINGS

When an investor coalition seeks to influence the environmental and social (E&S) responsibility of an investee company, how does the group’s leadership structure impact success on key dimensions?

The growing focus on E&S issues has meant more pressure on businesses in these areas from institutional shareholders. But scholarly work on how the structures of such engagements affect their E&S- related success and the performance of investors and investees has remained limited.

The authors address this by studying coordinated, cross-country E&S engagements and outcomes. They hypothesize that engagements with leaders that signal their commitment to the effort—through devotion of resources—and hold informational and reputational assets will promote greater success than engagements without leaders. They test this on a sample of 31 projects coordinated through the UN-supported Principles of Responsible Investment network and targeting 960 publicly listed firms.

While 52.7% of all engagements were successful, those with a clear leader were 23-31% more likely to succeed in driving E&S change. Coalitions with leaders holding informational advantage and reputational credibility were more likely to succeed. Both investor and target firms experienced post-engagement financial benefits as well. The results suggest coordinated E&S engagements—especially those with clear leadership— achieve their objectives while contributing to shareholder value.

The Impact of Coordinated E&S Engagements

As the importance of environmental and social (E&S) issues grows globally, investors have launched myriad initiatives to pressure businesses to act responsibly. Scholars have argued that “voice” (engagement) with investee companies is more effective than exit/divestment. But there has been only limited research on the structure and success of coordinated, collaborative, cross-country attempts to influence E&S- related behavior.

The authors work to fill this gap through research on the structure of such engagement strategies, with focus on understanding the impact of patterns of coalition-formation and leadership on success rates and financial outcomes. Specific measures include those related to leadership characteristics and mechanisms (informational and reputational advantages) and target-firm returns (stock returns and return on assets).

Central to the research is a previously established economics of leadership framework—specifically, that coalition dynamics unfold in two main scenarios: with and without a leader, whether an individual or organization. The argument is that coalitions with leaders who have superior information and “lead by example”—and signal their commitment through use of resources—will perform better than coalitions without leaders. The authors apply this proposition to E&S engagement efforts by coalitions of shareholders.

A Study of PRI-Coordinated E&S Engagements

The researchers studied engagement efforts coordinated by institutional investors through the Collaboration Platform provided by the Principles of Responsible Investment (PRI), the UN-supported largest global network for investors committed to corporate responsibility and sustainable returns.

The data included coordinated engagement projects initiated between 2007 and 2015 by 224 investment organizations. These collaborators—investment managers, asset owners, and service-providers from 24 countries—targeted 960 publicly listed firms, with an average of 26 investors per engagement and a duration of about two years. Among the engagements, 15 had lead organizations.

The researchers tapped PRI and multiple other sources for information on coalition members, target firms, engagement success, and pre- and post-engagement performance on financial measures including returns and fund flows.

E&S Engagement Leadership Promotes Success on Multiple Dimensions

The work yielded multiple results with meaningful implications for investors’ E&S influence efforts.

Overall, the average rate of success across engagements in the sample was 52.7%. As predicted, engagements with clear leadership were 23-31% more likely to be successful in driving E&S change in target firms, an economically significant finding.

Leaders were more likely to be investment managers, and leaders tended to have formal internal engagement processes and to participate in other collaborative initiatives—characteristics that acted as signals of their ability to lead E&S engagements, consistent with the idea of leading by example through resource-intensive effort.

As far as mechanism, engagements with leaders holding an informational advantage—as represented by the leader’s location in the same country as the target firm—were more likely to succeed, as were those led by leaders with a strong reputation, as measured by repeated interaction between the leader and followers in the coalition.

Moreover, both investor and targeted firms benefited from engagements driven by coalitions with clear leaders: investors enjoyed increased fund flows; target firms experienced an average increase in annual abnormal buy-and-hold stock returns of 4.7% and in annual return on assets of 0.9% in the first two years following engagement initiation, with those growing to 9.4% and 2.3%, respectively, by the third year. Engagements with no leader resulted in no changes in these measures for target firms.

Overall, the findings suggest that coordinated E&S engagements achieve their objectives in a large proportion of cases without compromising investment returns. Indeed, PRI-coordinated activities are shown to contribute to shareholder value, and should be headed by a credible leader to maximize outcomes.

KEY DATA

PRI-coordinated E&S engagements reflecting UN Social Development Goals in Environmental, Social, and Governance areas

Coalition members/roles and target firms (from PRI data)

Success of engagement (from PRI records, with varying criteria such as scorecards related to policy and implementation pre- and post-engagement)

Target-company attributes and performance (PRI, WorldScope/Compustat, MSCI country return index, and other data)

Leader firm fund flows (FactSet data)

PRACTICAL IMPLICATIONS

Coordinated E&S engagements are largely successful in driving meaningful change in responsible policy, implementation, and other activities among target firms—along with financial benefits for coalition leaders and target firms. Coalition leadership characteristics predict likelihood of success, meaning everyone can win from well- structured engagements.

Institutional investors seeking to engage with investees around E&S can work to maximize the likelihood of success by leading or joining shareholder coalitions. There should be a leader that signals substantial commitment of resources to the effort and has an informational advantage and reputational credibility, probably underpinned by geographic and cultural proximity to the target company.

The best leader of an engagement is not simply making a moral decision. They will also have an economic motivation and more “skin in the game” than other investors, along with the ability to deploy key resources toward the engagement. The motivation may help the institution achieve its objectives and increase future fund flows

Please access the original research brief here.

US Sustainable Investing Trends 2024-2025

The US SIF Trends Report 2024/2025 provides a comprehensive understanding of the trends driving $52.5 trillion in US assets under management (AUM), including $6.5 trillion explicitly marketed as ESG or sustainability-focused investments.

Key Findings and Takeaways

The Market is Poised for Growth

73% of survey respondents expect the sustainable investment market to grow significantly in the next 1-2 years, driven by client demand, regulatory evolution, and advances in data analytics. This is still the case, despite political headwinds and regulatory scrutiny.

Stewardship Takes Center Stage

79% of US market assets ($41.5 trillion) are now covered by stewardship policies, though further research is needed to assess their active implementation and impact.

Focus on Climate and Clean Energy

Climate change remains the dominant theme, with a strong emphasis on clean energy transitions, carbon reduction, and nature restoration.

Strategic Shifts in Investment Approaches

ESG integration (81%) and exclusionary screening (75%) are the most commonly used strategies. Survey responses indicate that 62% use 5 or more negative screens.

Challenges and Opportunities Ahead

Political challenges, such as anti-ESG rhetoric and greenwashing concerns, continue to shape the narrative. Our survey shows that although these present challenges, they also highlight the need for improved communication and education about the value of sustainable investing.

Access the detailed report on US SIF’s website.

Proxy Review 2025

2025 Proxy Season Executive Summary

This year, shareholders filed 355 environmental, social, and sustainable governance (ESG) proposals as of February 21, 2025. Additional proposals will be filed as the year progresses, but the shape of the 2025 spring annual meeting season is now clear.

The 2025 proxy season has seen a sharp drop in proposals filed from 2024, primarily due to the change in the presidential administration and what many expected to be a dramatic policy shift at the Securities and Exchange Commission (SEC).

Proponents have largely taken a “wait-and-see” approach, electing not to file resolutions until they were able to assess the direction of the new SEC. This approach was validated as it quickly became clear that some proposals that had been allowed by the SEC for decades, began to be omitted. And in a move that clearly undermined proponents—after the majority of the 2025 resolutions were filed, the SEC formally changed the rules of what could be excluded and extended the timeframe for companies to submit or amend their no-action filings without allowing shareholders the same opportunity

to amend their resolutions.

Another factor in the drop in filings is that more companies engaged in dialogue with shareholders in order to avoid both the need for proposals and the related publicity that could draw attention to them given the current political attacks on DEI and climate.

Next year, shareholders will, of course, revise their proposals to meet the new rules and it is anticipated that the number of filings will go up. Yet the larger political and legal attacks on sustainable investing, institutional investors, and proxy analysts does raises concerns that the SEC will take further actions to curtail shareholder rights and hinder shareholder proposals.

The total number of 2025 ESG resolutions are down 34% from 2024 when 536 such proposals were filed by this point. Average support for pro-ESG proposals in 2024 was 19.6%, down from 21.5% in 2023 and well below the 33.3% average vote of 2021. In 2024 there were fewer majority votes than we had seen in previous years. Again, much of the decline in votes is attributable to the large asset managers no longer supporting ESG proposals and the attacks on taking material ESG risks into account.

Thus far, 78 proposals in the 2025 proxy season – 22% of the total filed – were withdrawn. At a similar time in 2024, only 7.7% of proposals had been withdrawn. March and April often see a flurry of withdrawals before proxy statements are sent out, so it will be interesting to see if more companies elect to privately come to an agreement with or engage their shareholders in this incendiary political climate to avoid the public spotlight and how many resolutions are withdrawn to avoid being omitted under the new rules. On March 7, 2025, the SEC reported 221 proposals had received no-action requests. In 2024 there were 7 omissions and 94 no-action requests pending at a similar date.

For a more detailed report on the 2025 Proxy Season, access the resource here.

Letter from Democratic Financial Officers to Asset Managers Regarding Environmental and Social Issues

A coalition of 17 Democrat finance officials have sent a letter to executives at BlackRock and 17 other firms, pushing the institutions to reaffirm their commitment to managing long-term risks like climate change. Executives at Vanguard, State Street and JPMorgan Chase also received the Americans for Responsible Growth letter. The full list of recipients include Amundi, BNY, Capital Group, Fidelity Investments, Franklin Templeton, Geode Capital Management, Goldman Sachs, Invesco, Legal & General, Morgan Stanley, Northern Trust, Nuveen, T. Rowe Price and Wellington Management.

An excerpt from the letter to BlackRock is included below.

Dear Mr. Fink,

We write to offer a fundamentally different vision of fiduciary responsibility than the one advanced in the July 2025 letter to you from signatories of the State Financial Officers Foundation (SFOF).

We believe the views expressed in their letter misrepresent the true meaning of fiduciary duty and would require asset managers to take a passive approach to oversight while ignoring the nature of long-term value creation in modern capital markets. In contrast, we believe that fiduciary duty calls for active oversight, responsible governance, and the full exercise of ownership rights on behalf of the workers and retirees we serve.

Fiduciary duty, as properly understood, requires—not prohibits—investor consideration of material risks and long-horizon opportunities. Institutional investors, including public pension funds, are long-term owners. They bear the consequences of unmanaged risks—whether climate-related, governance-related, or supply chain-related—and must ensure that corporations and their boards address such risks with transparency and accountability.

Asset owners and their asset managers must retain and effectively use their authority to vote proxies, and engage companies to deliver durable, risk-adjusted financial returns over the long-term.

It is particularly unreasonable to suggest that asset owners whose portfolios span the entire economy should be barred from engaging the largest firms in the market. Today, the top 100 companies represent more than 70% of U.S. market capitalization. For many institutional investors, these holdings are structurally inescapable. Denying the right to engage with these companies is tantamount to severing ownership from stewardship.

We commend asset managers who are expanding opportunities for clients to vote proxies. We urge you to focus on empowering institutional investors and uphold an approach to fiduciary duty grounded in transparency, accountability, and long-term value creation. It is essential that you lead in developing tools and mechanisms that connect capital to oversight.

We invite you to respond by September 1, 2025, and to meet with our offices to reaffirm your current commitment to responsible stewardship and build a constructive dialogue around this issue.

The Democrat finance officials represent Connecticut, Delaware, Maine, Massachusetts, Minnesota, Nevada, New Mexico, Oregon, Rhode Island, Vermont and Washington. They are looking for firms to reach out to meet with their offices and reaffirm their “current commitment to responsible stewardship” by Sept. 1.

Sustainable Investment Markets: Evolution and Impact

How Investors Can Advance Sustainable Urban Development Through Innovative Financing Models and Climate Narratives in a Polarized Environment

Authors: Austin Ariss, Mariama Bah, Renata Gladkikh, Nanda Jasuma, Smita Samanta

Executive Summary

Policy volatility has become structural, not episodic, as evidenced by the 2025 $7B offshore wind rollback creating an operating environment without a reliable policy floor for sustainable investment.

Despite 58% of investment professionals prioritizing SDG 11, implementation lags due to a fundamental mismatch: capital is ready but execution is constrained by fragmented regulation, stakeholder complexity, and inconsistent incentives.

Our research reveals that successful urban sustainability investments pair mechanism with a message. Blended finance structures resolve technical barriers to scale, while economic reframing creates the political space required for implementation.

Case analyses demonstrate the dual approach delivers results: the NYC MTA’s staged decarbonization was achieved through climate bonds and strategic communication; affordable housing preservation funds yielded 14–24% IRR by aligning community and investor interests.

International experience confirms economic reframing decreases polarization: Australia’s natural capital approach positioned environmental protection as asset management; Japan’s energy security framing enabled nuclear revival despite post-Fukushima concerns

The difference between stalled climate finance and transformative sustainable investment lies in this integrated approach. For US SIF members navigating an uncertain policy landscape, this report offers a strategic toolkit focused on three actionable pathways: standardizing blended finance templates, aligning impact metrics, and repositioning climate initiatives as economic utility to create resilient investment pathways rather than waiting for ideal policy conditions.

Health and Safety in the Fast Food Industry

MIKAIL HUSAIN, ESG Analyst, SOC Investment Group

LOUIS MALIZIA, Corporate Governance Director, SOC Investment Group

In recent years, the food service industry has been rife with workplace health safety issues. Food service workers have been attacked, stabbed, shot, and killed by customers in the restaurants where they work. According to one study, between 2017 and 2020, at least 77,000 violent or threatening incidents took place at California fast-food restaurants. Recent data indicate that the cost of workplace violence could be as much as $56 billion annually – and that’s likely an undercount. However, workplace health and safety issues are not limited to customer violence. Workers have also been made to work under unsafe and unsanitary conditions, such as restaurants with high kitchen temperatures and restaurants infested with vermin.

These issues and the media response they elicit are clear operational and reputational risks for the companies, which can lead to difficulties with staff retention in an industry with high turnover. According to the U.S. Chamber of Commerce, the food service and hospitality industry has a consistently high “quit rate.” Understaffing at fast food restaurants can lead to longer wait times for customers, diminished employee productivity, and an increase in safety hazards. Workplace health and safety issues in fast food restaurants have led to worker strikes and protests of working conditions, as well as fines and temporary restaurant closures imposed by regulators.

Why should investors care? If left unaddressed, workplace health and safety issues can expose companies and their shareholders to unnecessary risk. In recent years, shareholders have recognized the risks posed by workplace health and safety issues and are pressing companies to take more action to address them. In 2023, Dollar General shareholders demonstrated this with a majority vote in support of a health and safety audit proposal.

To address these risks, SOC Investment Group has filed health and safety audit proposals at McDonald’s, Yum! Brands, Restaurant Brands International, and Chipotle for the 2025 proxy season. The proposals are similar to the proposal we filed last year at Chipotle, which received 30% support from shareholders, well above the average support level of 18% for social proposals in the S&P 500 in 2024. The resolution requests that the companies’ boards of directors commission an independent third-party audit on the impact of company policies and practices on the safety and well-being of workers throughout company-branded operations.

We believe any relaxation of safety standards in pursuit of short-term benefits creates risks for workers, customers, and shareholders and may result in long-term reputational damage that can be difficult to reverse. In addition to these risks, companies that neglect health and safety in the short term may face increased regulatory and business risks that can erode margins and reduce long-term shareholder returns.

Human Rights & Artificial Intelligence

BRANDON REES, Deputy Director, Corporations and Capital Markets, American Federation of Labor and Congress of Industrial Organizations (AFL-CIO)

The widespread adoption of artificial intelligence (AI) by companies has the potential to unleash broad-based economic prosperity by enhancing employee productivity. But, it also carries risks to workers’ rights as AI algorithms increasingly set productivity quotas, make human resource decisions, and direct workers on how to perform their jobs. For example, the use of AI in human resources decisions can result in unlawful employment discrimination.

According to the UN Guiding Principles on Business and Human Rights, companies have an international obligation to “know and show” that they respect human rights. In using this due diligence framework to manage AI-related human rights risks, companies should: 1) be transparent about how AI is used by the company, 2) establish board-level oversight and monitoring of AI-related risks, and 3) give workers a voice in how AI is used in the workplace.

First, companies should be transparent with how they use AI in their business operations. Investors are regularly engaging with their portfolio companies about AI as part of their stewardship activities. Many companies are now voluntarily disclosing information on how they use AI to their investors, employees, and customers. By addressing the ethical considerations of AI in a transparent manner, companies can build trust with their stakeholders.

Second, boards of directors have an important role to play in monitoring and managing AI risks. Under the Caremark standard in Delaware corporate law, directors have a fiduciary duty to oversee their company’s operations by establishing an internal reporting system. At a minimum, companies adopting AI into their business operations need to establish board-level oversight of the risks involved and report on any regulatory noncompliance issues that arise.

And, finally, companies should view AI as an opportunity to enhance human decision-making by their employees, not as a substitute. Companies that view their workers as partners in implementing AI are more likely to attract and retain a motivated workforce and realize the productivity gains that AI promises. Unions are the best way for workers to negotiate how AI technology should be implemented in the workplace.

To address these concerns, the AFL-CIO Equity Index Funds have introduced shareholder proposals that ask companies to commission an independent, third-party human rights assessment of their use of AI. Proposals are expected to go to a vote at Amazon and Lyft in 2025, and similar proposals requesting a transparency report on the use of AI received high levels of shareholder support at Apple (37%) and Netflix (43%) in 2024.

Nature is Critical to Business

ANDREW SHALIT , Shareholder Advocate, Green Century Capital Management

Global biodiversity is deteriorating faster than at any time in human history, largely due to human activity. Such massive biodiversity loss poses serious economic and financial risk as more than half the world’s economy is moderately or highly dependent on nature. To reverse this trend, companies must start by meaningfully assessing, disclosing, and addressing their nature-related impacts, dependencies, risks, and opportunities.

Green Century has long worked to advance protections for nature through our work to preserve natural forests, reduce the use of harmful chemicals, and put companies on a path to net zero emissions. In the fall of 2023, we filed our first proposals that specifically address biodiversity, asking companies including PepsiCo and Kellanova to complete material biodiversity dependency and impact assessments. This year, we refiled our resolution at PepsiCo and co-filed, along with Proxy Impact, a biodiversity and nature disclosure resolution at Home Depot, led by Domini Impact Investments. These resolutions call on companies to face and address the challenges to nature that threaten the products they sell and the markets in which they operate.

We also filed a biodiversity resolution at Chemours, a chemical company that mines titanium to create products that whiten our paint, toothpaste, and sunscreen. While titanium is a plentiful mineral, Chemours conducts some of its mining operations in ecologically sensitive areas. Our proposal asks Chemours to adopt a policy to assess any reasonably likely irreversible impacts on biodiversity prior to commencing mining operations in ecologically sensitive areas, as well as any related financial, reputational, and operational implications for the company should those impacts occur. Bottom line, it probably doesn’t make financial sense to mine ecologically sensitive areas for a natural resource you can easily find elsewhere – and it’s at least worth assessing those risks and impacts first.

Global institutions have begun to recognize the need for action on nature. In 2022, 196 countries ratified the Global Biodiversity Framework, setting out ambitious goals to protect and restore nature. The Taskforce for Nature-Related Financial Disclosures (TNFD) was launched in September 2023. As of this writing, 546 organizations worldwide have committed to assessing and disclosing under TNFD, including 346 corporations and 139 financial institutions. The Global Reporting Initiative, CDP, and Science Based Targets Network are developing support for biodiversity and nature disclosure and target setting. Biodiversity disclosure is also included in the EU’s Corporate Social Responsibility Directive. Industry groups, including the Finance for Biodiversity Foundation and Business for Nature, provide additional support for companies seeking to transition to nature-positive practices.

We can no longer take nature for granted. Companies must find nature-positive approaches to all aspects of their business, from supply chains to manufacturing to distribution, to avoid near- and long-term risks associated with the degradation of the natural world. Investors have a crucial role to play by insisting that companies take concrete steps to address the systemic risk of global biodiversity loss.

For more details on biodiversity and nature related proposals from the 2025, access 2025 Proxy Preview.

2025 Update on SEC Guidance for Shareholder Proposals

SANFORD LEWIS, Director and General Counsel, Shareholder Rights Group

In order to help companies and investors determine whether a shareholder proposal qualifies to appear on the proxy statement under SEC Rule 14a-8, the SEC has developed a process to allow companies to inquire in advance whether a proposal must be included. The “no action” process is an informal review process through which the SEC staff advises companies and their investors on whether the SEC staff would recommend enforcement action if a company fails to include a submitted shareholder proposal on its annual proxy statement.

The SEC staff periodically recalibrates its interpretation of the rules as it applies in the no-action process to reflect current issues of concern to investors and companies. For example, in 2021, the SEC staff issued an interpretive bulletin, Staff Legal Bulletin 14L, which clarified the interpretation of ordinary business and micromanagement rules.

The bulletin was subject to pushback from issuers and asset managers. Trade associations, such as the National Association of Manufacturers and Business Roundtable, were critical of the bulletin, asserting that it no longer required that a proposal address an issue that is significant to the company receiving it. Asset managers who vote on shareholder proposals asserted that proposals were becoming too prescriptive.

In 2023 and 2024, following the market response and criticisms, the staff tightened up its interpretations of the micromanagement rule and excluded many proposals on social and environmental issues that had previously been allowed. From November 1, 2023, to May 1, 2024, the SEC staff supported company requests for exclusion of proposals roughly 68% of the time, similar to the average exclusion rate during the first Trump administration, from 2017 to 2020, which was 69%. In 2025, the staff has again tightened its interpretation of the micromanagement rule, excluding, for example, proposals on lobbying disclosure that had previously been permissible since at least 2011.

On February 12, 2025, the SEC staff issued Staff Legal Bulletin 14M to signify a more restrictive posture on proposals that request specific forms of disclosure or actions by companies. The bulletin revoked Staff Legal Bulletin 14L and altered staff interpretations of the micromanagement, ordinary business, and relevance exclusions.

The new bulletin requires that assessment of whether a shareholder proposal transcends ordinary business should be evaluated by looking at the significance of the proposal to the particular company that receives the proposal.

The new bulletin also shifts interpretation of micromanagement from Staff legal Bulletin 14L’s clear guidelines, toward a more subjective staff evaluation as to whether the proposal seeks a specific method, strategy, or outcome that the staff views as more appropriately determined by the board or management. Such new interpretations are anticipated to lead to an increase in the exclusion of environmental and social proposals and fewer such proposals appearing on proxy statements.

In a letter submitted on February 18, representatives of the Shareholder Rights Group, the Interfaith Center on Corporate Responsibility, and As You Sow requested that the SEC refrain from applying the guidance to shareholder proposals filed prior to the issuance of the bulletin: “Shareholders rely on Staff guidance regarding the shareholder proposal process when engaging the management of the companies they own. By filing proposals that adhere to the guidance, shareholders are able to present proposals more likely to conform to Staff understanding of the exclusions in Rule 14a-8. This streamlines the process for investors, companies, and the Staff. Applying new guidance to previously submitted proposals would unfairly penalize investors who followed the extant guidance in good faith, believing that they were following the procedures that would lead to clear results, limiting the need for the costly back and forth of the no-action process.”

Along with new regulatory guidance from the SEC, the investor right to file shareholder proposals has also come under attack from legislation in Congress and lawsuits filed in the federal courts in Texas. The new report, Shareholder Proposals: An Essential Investor Right, offers a detailed and thoughtful defense of shareholder proposals. It catalogues their role in creating a powerful public platform for challenging and improving corporate policies, practices, performance, and impacts and providing an important mechanism for surfacing investor perspectives on material issues. The report further demonstrates how shareholder proposals have enabled investors to safeguard their portfolios from risks and protect the American public by helping to catalyze positive corporate change on an array of issues.

Avocado-driven Deforestation in Mexico

The Avocado Industry’s Turning Point: How Corporate Accountability Is Reducing Deforestation in Mexico

In complex situations where environmental and human rights issues driven by a high-impact commodity are not adequately addressed by local regulation, corporations have the power to demand more from their suppliers. When this influence is directed properly, corporations can catalyze significant positive change for all stakeholders. This is demonstrated in the continuing evolution of Mexico's avocado industry, where shareholder engagement, political action, NGO efforts, and community organizing are helping corporations to address rampant illegal deforestation and its impacts.

Our insatiable demand for avocados has created serious environmental and social issues for Mexico. More than 10 football fields of Mexican forests are cleared daily for avocado orchards, with most of this deforestation violating federal law. Illegal deforestation has severe consequences: depleting community water supplies, destroying protected habitats including the Monarch Butterfly Biosphere Reserve, and enabling criminal activities through land seizures and corruption.

In 2023, a powerful New York Times exposé based on a Climate Rights International (CRI) report lifted the veil on the dark side of the avocado industry, exposing illegal practices that have been wreaking havoc on Mexico’s forests and communities for years. The CRI report reviewed satellite images of the same land over time to identify where unpermitted deforestation had occurred. Using that data, avocados from major importers could be traced back to orchards on illegally deforested lands, calling into question the sustainability of a substantial portion of the avocados sold in U.S. supermarkets.

The NYT exposé prompted a reaction. Environmental NGOs began to put pressure on policy makers and grocery chains to address avocado-driven deforestation. In February 2024, six U.S. senators urged the Biden Administration to support efforts to ensure that the US-Mexico avocado trade is not driving illegal deforestation. This collective call to action coincided with the 2024 Super Bowl, prompting action from Michoacán's governor and Mexico's agricultural secretary.

Noting this growing risk, As You Sow began engaging with leading U.S. retailers and distributors of avocados, raising awareness of illegal deforestation in their avocado supply chains and highlighting the practical solution sanctioned by the State of Michoacan: a system to trace and flag illegal orchards and a transparent certification system. Working with Guardián Forestal, a Mexican NGO specializing in GPS data, the State of Michoacan has created an online portal to verify avocado sourcing. The system is elegantly simple: orchards established before 2018 are considered legal - accounting for the six-year growth cycle of avocado trees - while newer orchards without federal permits are flagged as illegal.

The impact of the certification system was immediate and profound. By approaching the issue from both the top down and the bottom up, As You Sow worked with Mission Produce, a major avocado supplier, which committed to avoid the purchase of avocados from illegally deforested orchards. This was soon followed by certification commitments from other major avocado suppliers recognizing the system as a way to ensure ethical sourcing while protecting the environment.

Other retailers and distributors now have the opportunity to not only leverage this verification system to avoid illegal deforestation in the Michoacan avocado market, but to seek expansion of the tool to other Mexican states. By ensuring avocados aren’t coming from recently deforested land, companies can help disincentivize further deforestation in the region.

Solution-oriented action can solve the world’s toughest environmental and social issues. The collective action on avocado driven deforestation provides a blueprint for how industries can work through complex challenges and champion solutions for lasting and meaningful change.

Large Institutional investors Respond to the Proxy Voting Debate

This article draws from Dorothy S. Lund’s scholarly work, “The Past, Present, and Future of Proxy Voting Choice,” which surveys the evolution of U.S. proxy voting policies and details recent reforms by major index fund managers in response to political and public scrutiny.

The role of BlackRock, Vanguard, and State Street in U.S. markets has changed dramatically over the past two decades. Together, these managers hold massive stakes in most public companies and have become central players in corporate governance. This concentration, combined with the rise of index funds, prompted a lively policy debate: should a handful of big asset managers wield so much voting power?

Under pressure from policymakers and clients, especially on high-profile issues like ESG (environmental, social, and governance), these firms have responded by rolling out voting choice programs. BlackRock’s and State Street’s initiatives now allow a significant portion of institutional and some retail fund investors to guide votes based on selected policy templates. Vanguard has joined as well, expanding access to similar options.

While these programs do not yet put all voting power in the hands of individual investors, they provide new flexibility. Investors can opt into policies that match their priorities or values, such as sustainability or corporate governance best practices. The effectiveness and reach of these programs are still developing, but for the first time, a broad base of fund holders is participating, even if only indirectly, in corporate decision-making.

For example, board diversity is a common proxy voting topic where investors' preferences may vary. BlackRock’s 2025 proxy voting guidelines reflect a case-by-case approach to diversity voting decisions, removing rigid numerical targets but still emphasizing diversity’s importance relative to market norms.

Through BlackRock Voting Choice, institutional and eligible retail investors can now direct their pro-rata share of votes or select from third-party voting policies that might be stricter or more lenient on board diversity issues than BlackRock’s default policy. This means an investor who prioritizes board diversity could opt into a voting policy that votes against boards lacking sufficient gender or racial diversity, while another investor might choose a policy that applies a different threshold or focus.

This flexibility exemplifies the practical impact of voting choice programs: empowering investors to exercise their governance preferences on specific topics such as diversity, while still investing through large index funds. It also demonstrates how the Big Three are adapting governance oversight to evolving political and client demands.

What Is Proxy Voting Choice?

This analysis is based on Dorothy S. Lund’s 2025 article, “The Past, Present, and Future of Proxy Voting Choice,” published in the Journal of Corporation Law and available via Columbia Law School’s Scholarship Archive. Lund examines how new proxy voting systems have emerged as a response to concerns about the concentration of voting power among a small group of U.S. asset managers, especially the “Big Three”: BlackRock, Vanguard, and State Street.

Proxy voting allows shareholders to cast ballots on important issues at corporate annual meetings, and in recent years, several large asset managers have begun offering clients new choices in this process. “Proxy voting choice” is an innovation where funds give end investors—both institutional and, more recently, retail—the option to influence or directly choose how their shares are voted.

Traditionally, investment managers like BlackRock, Vanguard, and State Street controlled the voting rights for the millions of shares pooled in their investment funds. As these firms grew, concerns mounted about the concentration of voting power among just a few institutions. Critics pointed out that passive index funds have limited incentives to thoroughly research and vote on individual companies, potentially weakening effective corporate oversight.

In response, and after growing public and political pressure on topics like climate change and diversity, asset managers began creating “voting choice” programs. These let clients select from several third-party voting policies or the fund’s default approach. The approach is still voluntary and in its early stages, but millions of investors now have access to some form of voting participation—an important shift in how American corporate governance works. Participation rates and ultimate impacts remain to be seen, but proxy voting choice marks a major step toward democratizing shareholder voice in large public funds.

For example, BlackRock launched its Voting Choice program in 2022, which allows eligible clients—including institutional and some retail investors—to select from a menu of third-party voting policies or use their own. The program has expanded rapidly and now covers $2.7 trillion in index equity assets. More information is available on BlackRock’s official Voting Choice page

Similarly, State Street offers a Proxy Voting Choice program that permits eligible investors in institutional index funds and certain ETFs to decide how their pro-rata share of votes is cast. The program includes access to several third-party voting policies and continues to expand across eligible funds. Details can be found at State Street’s proxy voting page.

To access the full article, please click here.

Responsible Investment Requires a Proxy Voting System Responsive to Retail Investors

There is growing awareness amongst retail investors of the importance of environmental, social, and governance (ESG ) factors to the performance of their stocks. The same factors impact their lives from a broader societal and economic perspective. Institutional investors have incorporated ESG issues into their proxy voting and corporate engagement. Retail investors who invest in stocks directly have the same voting rights, and collectively a similar power, but data shows that their voting rates have declined precipitously over the past forty years. This chapter traces the history of property rights and proxy voting, examines them within the current regulatory context, and posits that economic rights have been well protected but ownership rights have been neglected. An established framework for stages of capitalism is re-imagined, situating retail investors’ disengagement from the proxy process and highlighting suggestions to regulators for addressing the proxy voting gap.

To read the full paper, please go to SSRN’s website.

University of Oxford

Corporate Support for DEI Continues Among Investors and Companies

August, 2025

During this proxy season, companies faced a wave of shareholder resolutions attacking diversity, equity, and inclusion (DEI) programs and calling for their eradication. This campaign expanded on last year’s anti-DEI attacks, as tracked in the “Championing Diversity in Corporations," which also included quotes from numerous companies strongly defending their diversity programs. This year’s anti-DEI resolutions built upon growing attacks on DEI by various government agencies and right-wing critics, who argued that company diversity programs were on the way out. Interestingly, these anti-DEI resolutions conveyed the exact opposite message, demonstrating that investors and companies alike believe that diversity has a positive impact on employees and long-term shareholder value.

In fact, in this proxy season, approximately 98% of the shares voted to maintain current corporate diversity, equity, and inclusion programs. Companies including Disney, Costco, Visa, Apple, Deere, Boeing, Goldman Sachs, Levi’s, AMEX, Coca-Cola, Berkshire Hathaway, Bristol Myers, and Gilead Science saw near-unanimous votes, averaging a mere 2% shareholder vote supporting these resolutions, sending a clear message to the boards that shareholders support the business case for non-discrimination in employment and a diverse workforce.

Many of these companies under attack remained publicly committed to their longstanding DEI programs. Corporations like Costco, JPMorganChase, Delta Air Lines, American Airlines, Southwest Airlines, and Apple continue to view diversity as a cornerstone of their workforce strategies, refusing to back down despite mounting pressure from conservatives.

These companies fully understand the benefits of having diverse teams and leadership. For example, a review by As You Sow and Whistle Stop Capital of over 1,600 companies found that manager diversity is positively associated with key financial performance indicators, including return on equity and invested capital, revenue growth, and share price performance.

Similarly, a recent investor brief by the Canadian organization SHARE found that diversity, equity and inclusion add to company performance and, therefore, shareholder value. If a company eliminates or dilutes efforts to promote diversity, they are neglecting that benefit and adding risk for investors. Simply stated, the data shows that diversity is good for business.

The following is an excerpt from a series of quotes and public statements from Senior executives on DEI. This is a small snapshot of company statements, but it clearly demonstrates the fact that numerous leading corporations strongly resist these attacks and stand behind their commitment to non- discrimination and diversity. At the end we also include relevant articles.

AMERICAN EXPRESS:

"We Embrace Diversity: We believe that diversity of experiences, perspectives, and backgrounds enables us to be our best."

BOEING

“Boeing remains committed to recruiting and retaining top talent and creating an inclusive work environment where every teammate around the world is respected, valued, and empowered to succeed," and defended its "culture of nondiscrimination, inclusion, and meritocracy."

COCA-COLA

"Creating a culture of diversity, equity and inclusion. Diversity, equity and inclusion are at the heart of our values and our growth strategy and play an important part in our company's success."

GOLDMAN SACHS

“We run an inclusive organization, and we’re going to continue to run an inclusive organization.” - David Solomon, CEO, Goldman Sachs

JPMORGANCHASE

“We will continue to reach out to the Black community, the Hispanic community, the veteran’s community, and LGBTQ. We have teams with second chance initiatives — governors in blue states and red states like what we do.” - CEO Jamie Dimon in a CNBC interview.

MICROSOFT

“If ever there were a critical time for the business case for diversity and inclusion in the workplace, it is now… Our innovation has come from our commitment to Diversity and Inclusion (D&I), and our future innovation depends on D&I.”

To read the full article, please click here.

This document was drafted by Maxwell Homans, Shareholder Advocacy Associate, Mercy Investment Services, in partnership with Tim Smith, Senior Policy Advisor, ICCR.

SEC Increases Exclusion of Proposals - 2023-2025

In order to help companies decide whether a proposal passes these tests, the SEC has developed a process to allow companies to ask the SEC in advance whether a proposal must be included in the meeting materials. The “no action” process is an informal review process through which the SEC staff advises companies and their investors on whether the SEC staff would likely recommend enforcement action if a company fails to include a submitted shareholder proposal on its annual proxy statement. The staff grants the company’s request if it finds some basis to agree with the company’s arguments that the proposal is excludable under one of the elements of SEC Rule 14a-8. It denies the request if it is unable to concur with the company’s arguments.

SEC Rule 14a-8 is intended to exclude trivial, irrelevant, and inappropriate shareholder proposals, thus minimizing the burden on companies. The no action process is a structured, time-tested process that adds an additional layer of objective scrutiny to company decisions regarding whether to include or exclude proposals, which serves to protect investors’ interests. If an investor disagrees with the no action decision by the SEC, the investor can submit a letter in opposition, but it does not have legal recourse against the SEC. Without Rule 14a-8 and the no action process, an investor only has the option to sue the company under federal law if it disagrees with a company’s decision to not place a proposal on the proxy, which would add delays, and significant costs for both parties.

The SEC staff periodically recalibrates its interpretation of the rules of the no action process to reflect current issues of concern to investors and companies. For example, in 2021, the SEC staff issued an interpretive bulletin, Staff Legal Bulletin 14L, which clarified ordinary business and micromanagement rules in a manner that allowed some environmental and social proposals to reach the proxy that might not have qualified in a prior interpretation. However, following market response and criticisms, the staff tightened up its interpretations of micromanagement and excluded many proposals on social and environmental issues that had previously been allowed, even with the new bulletin remaining in place. From November 1, 2023 to May 1, 2024 the SEC staff supported company requests for exclusion of proposals roughly 68% of the time, similar to the average exclusion rate during the first Trump administration, from 2017-2020, which was 69%.

In the 2025 proxy season, the staff again tightened its interpretation of the micromanagement rule, excluding, for example, proposals on lobbying disclosure that had previously been permissible since at least 2011. On February 12, 2025, the SEC staff signified that it is taking a more restrictive posture on proposals that request specific forms of disclosure or actions by companies. SLB 14M issued on that day revoked SLB 14L and altered staff interpretations of the micromanagement, ordinary business and relevance exclusions. The new interpretations led to an increase in the exclusion of environmental and social proposals, and fewer such proposals appearing on proxy statements. Of particular note in SLB 14M is a shift in interpretation of micromanagement from SLB 14L’s focus on the interest and capacities of shareholders to understand and vote on an advisory proposal, and toward an evaluation as to whether the proposal seeks a specific method, strategy or outcome that the staff views as more appropriately determined by the board or management.

When Public Sentiment Drives Shareholder Strategy

How headlines, hashtags, and media cycles are reshaping proxy season

Do public opinion and media narratives really influence shareholder proposals? A new study says: yes, and in some cases, that influence is financially material.

Analyzing proposal volumes and public discourse, the authors find that:

Increased public salience of corporate issues (like AI ethics, reproductive rights, or climate impacts) correlates with a rise in ESG-focused proposals;

These proposals are more likely to receive broader investor support when they align with media attention and reputational risk;

And when companies respond constructively, firm value tends to improve.

📉 Sentiment as an Early Warning Signal

For investors, public opinion is often a precursor to regulatory or reputational risk. Think of social movements that preceded litigation, consumer backlash, or regulatory intervention—public scrutiny often arrives before the balance sheet feels the impact.

This study confirms that investor engagement is increasingly attuned to reputational signals and that media awareness serves as a “soft metric” for materiality.

“In today’s democratized information environment, companies can no longer operate behind closed doors, shielded from public scrutiny. Shareholders, armed with public sentiment data, are increasingly willing to hold management accountable. This new reality underscores the importance of transparency and responsiveness in maintaining investor trust and long-term value creation. ”

These insights have significant implications for both corporate leaders and investors. For management, the warning is: ignoring public sentiment can lead to increased shareholder activism and leadership turnover. For investors, our findings highlight the effectiveness of acting with the public’s voice in leading to corporate change.

Refer to the original article here.

Shareholder Voting and Corporate Governance

Why shareholder voting isn’t just symbolic—it’s structural

It’s easy to take shareholder voting rights for granted. But according to David Yermack (2010), voting is not just a procedural ritual—it’s a foundational component of corporate accountability.

Yermack’s comprehensive review of governance literature demonstrates that strong voting rights correlate with better corporate outcomes, including:

Lower CEO entrenchment,

Greater board independence,

More responsive management,

And ultimately, improved long-term firm performance.

These effects are especially visible in firms where shareholders have actively used proposals or majority voting to reshape governance policies. This article reviews recent research into corporate voting and elections. Regulatory reforms have given shareholders more voting power in the election of directors and in executive compensation issues. Shareholders use voting as a channel of communication with boards of directors, and protest voting can lead to significant changes in corporate governance and strategy. Some investors have embraced innovative empty voting strategies for decoupling voting rights from cash flow rights, enabling them to mount aggressive programs of shareholder activism.

🛠️ Voting Rights as Investor Tools

Proposals to declassify boards, require majority voting for directors, or separate the CEO and chair roles aren’t just governance “theater.” They are functional tools that:

Enable greater transparency,

Shift power away from entrenched insiders,

And reinforce the board’s accountability to long-term owners.

⚠️ A Warning Against Restriction

Yermack cautions that undermining shareholder voting mechanisms—whether by limiting proposal access or weakening vote influence—reduces a key market check on managerial behavior.

As policymakers revisit the rules around 14a-8, Yermack’s work offers a timely reminder: Shareholder voting is governance. Curtailing it risks undercutting the integrity of the capital markets themselves.

📚 Further Reading- Shareholder Voting and Corporate Governance