Rulemaking Petition-Factsheet

Formal Petition Regarding Amendments to Rule 14a-8

Under the Securities Exchange Act of 1934, Filed with the U.S. Securities and Exchange Commission, July 23, 2026

WHAT THE PETITION REQUESTS

The petition is filed under an SEC rule that invites shareholders to recommend changes to an SEC rule. The Petition asks that, if the SEC conducts a rulemaking on Rule 14a-8, it recalibrate rather than dismantle the rule. If the Commission proceeds with rulemaking, the petition reminds the SEC of its obligation under the Administrative Procedure Act to rigorously evaluate less harmful alternatives before any wholesale change.

NO ACTION PROCESS RECOMMENDATIONS

The no-action process be retained with reforms to sharpen the review process machinery—clarifying timelines, promoting direct engagement between issuers and proponents, and thereby reducing unnecessary demands on Commission staff:

establish a two-week engagement period after an issuer submits a notice of intent to exclude a shareholder proposal, during which the issuer and proponent may seek an agreement that potentially eliminates the need for a staff advisory opinion

provide specific timeframes for proponents to respond to exclusion notices, and confirm that the staff will consider any timely proponent response when issuing an advisory opinion;

extend the deadline for filing exclusion notices from 80 to 90 days, and clarify that the deadline runs from the earlier of the issuer’s proxy print deadline or its EDGAR filing deadline for the definitive Form DEF 14A; and

Set clear timeframes for a proponent to respond if a company requests a staff advisory opinion.

Allow 14 business days for responses to procedural objections such as proof of ownership, and 30 calendar days for responses to substantive exclusions

Eliminate outdated paper copy submission requirements.

Excise obsolete language in the existing Rule requiring the submission of six paper copies, reflecting the modern reality that all submissions are processed electronically.

RECOMMENDATIONS ON EVALUATING LESS HARMFUL ALTERNATIVES

In the event that the SEC proposes reforms to the shareholder proposal rule beyond the no action process, the petition reminds the SEC of its obligation to consider less harmful alternatives that would do less to disrupt the expectations and systems that the market has come to rely upon. Such less harmful alternatives could include retaining the federal framework while leaving dispute resolution to the courts and evaluating the related cost of litigation that this approach would impose. Such evaluation would also consider approaches for reducing the subjectivity of the rules to reduce disputes between proponents and issuers.

Signatories of the petition

The signatories include New York State Comptroller Thomas P. DiNapoli and organizations: Ceres, For the Long-Term, the Interfaith Center on Corporate Responsibility, Shareholder Rights Group, and US SIF

Rulemaking Petition regarding Amendments to Rule 14a-8 Under the Securities Exchange Act of 1934

July 23, 2026

Vanessa A. Countryman, Secretary

U.S. Securities and Exchange Commission

100 F Street, NE, Washington, DC 20549-1090

I. Introduction

The undersigned submit the following pursuant to 17 CFR § 201.192(a) (Rule 192(a) of the Commission’s Rules of Practice) and Section 553 of the Administrative Procedure Act.

Petitioners request that the Commission, in any rulemaking to amend Rule 14a-8 under the Securities Exchange Act of 1934 (“the Rule”), largely retain the Rule, which has, over the course of many decades established and refined a balance among issuers, proponents, and the voting shareholders whose capital is at stake.

The petition addresses both the no-action process as well as the underlying exclusion and procedural rules. We urge that both be retained and staff review be restored effective immediately.

In particular, in any rulemaking we urge that the no-action process be retained with consideration of reforms to sharpen the review process machinery—clarifying timelines, promoting direct engagement between issuers and proponents, and thereby reducing unnecessary demands on Commission staff. The amendments would:

establish a two-week engagement period after an issuer submits a notice of intent to exclude a shareholder proposal, during which the issuer and proponent may seek an agreement that may obviate the need for staff review of the notice;

provide specific timeframes for proponents to respond to exclusion notices, and confirm that the staff will consider any timely proponent response when issuing an advisory opinion;

extend the deadline for filing exclusion notices from 80 to 90 days, and clarify that the deadline runs from the earlier of the issuer’s proxy print deadline or its EDGAR filing deadline for the definitive Form DEF 14A; and

update the Rule to eliminate the archaic requirement that submissions be filed in paper copies.

Petitioners also recognize that Chairman Paul Atkins has signaled his intent for the Commission to abandon its role as an informal “referee” of the excludability of individual shareholder proposals and that the Division of Corporation Finance has paused review of most no-action requests. Therefore, while the petitioners believe that the no-action process should be retained and fully reinstated, the petition urges that any rulemaking not seek to limit the Commission’s role via a heavy handed wholesale rescission or other aggressive modification to the Rule without first rigorously evaluating less harmful alternatives including (a) limiting no-action letters to contested exclusion notices or significant policy matters or using other mechanisms, including those recommended in the petition to reduce the role of the staff or (b) retaining or refining the federal procedural and exclusion rules but leaving consideration of the validity of exclusion decisions to the courts. In the event it proposes substantial modifications or rescission of the no-action process or other elements of the Rule, the Commission should evaluate the impacts and costs associated with increased litigation already evidenced during the 2026 proxy season suspension, and how the existing substantive exclusions and procedures would function in the absence of Commission staff engagement on a proposal-by-proposal basis.

II. Statutory Authority

The Commission’s authority to adopt the requested amendments derives principally from Section 14(a) of the Securities Exchange Act of 1934 and the Commission’s broad authority to regulate corporate proxy statements in the public interest and for the protection of investors. The Commission has repeatedly affirmed its authority to establish and refine Rule 14a-8 in its various rule-making releases including Proposed Amendments to Rule 14a-8 Under the Securities Exchange Act of 1934 Relating to Proposals by Security Holders, Exchange Act Release No. 34-12598 (July 7, 1976), 41 Fed. Reg. 29,982 (proposed July 20, 1976) (to be codified at 17 C.F.R. pt. 240); Amendments to Rule 14a-8 Under the Securities Exchange Act of 1934 Relating to Proposals by Security Holders, Exchange Act Release No. 34-20091 (Aug. 16, 1983), 48 Fed. Reg. 38,218 (Aug. 23, 1983) (codified at 17 C.F.R. pt. 240); Shareholder Proposals Relating to the Election of Directors, Exchange Act Release No. 34-56161 (July 27, 2007), 72 Fed. Reg. 43,488 (proposed Aug. 3, 2007) (to be codified at 17 C.F.R. pt. 240); Substantial Implementation, Duplication, and Resubmission of Shareholder Proposals Under Exchange Act Rule 14a-8, Exchange Act Release No. 34-95267 (July 13, 2022), 87 Fed. Reg. 45,052 (proposed July 27, 2022) (to be codified at 17 C.F.R. pt. 240).

III. Interest of Petitioners

Petitioners include pension trustees and asset owners and organizations whose members or funds include individual investors and institutional fiduciaries—with long investment horizons and legal obligations to beneficiaries that make active stewardship not merely a choice but a duty. Many have filed shareholder proposals, and not all take the same perspective. All have relied on the proposal process as a practical tool for engaging companies on material risks, including through voting on shareholder proposals.

IV. Shareholder Proposals and the Rule 14a-8 Framework

Shareholders of public companies can submit proposals for consideration at annual meetings, providing a formal mechanism to influence corporate governance, strategy, and risk oversight. This process, which provides investors with important information about issues being raised by fellow shareholders, is made effective through the SEC’s proxy rules, particularly Rule 14a-8 (“the Rule”), which requires disclosure of eligible proposals in a company’s proxy statement so that shareholders are apprised of matters under consideration during the upcoming meeting and have an opportunity to vote on them through the proxy process.

To qualify a proposal under the Rule, shareholders must meet specified ownership thresholds, hold shares for a defined period, and comply with procedural requirements such as submission deadlines and proof of ownership. Rule 14a-8 also establishes thirteen enumerated grounds on which companies may exclude proposals, designed to screen out proposals that would not be likely to be significant to investors. The exclusions include, among other things, proposals that fall outside proper shareholder authority under state law, relate to ordinary business operations, contain misleading information, duplicate or conflict with other proposals, lack relevance, have already been substantially implemented, or fail to meet resubmission thresholds. The burden of justifying exclusion of a proposal falls on the issuer receiving the proposal, which must submit to the Commission an explanation of its reasons. Rule 14a-8(g), Rule 14a-8 (j)(2)(ii).

V. Removing a “Cornerstone” would Destabilize Corporate Governance in the US

The Commission’s Spring 2026 Unified Regulatory Flexibility Agenda includes a rulemaking to modify Rule 14a-8.[1] The petitioners are aware that Chair Paul Atkins and Commission members have articulated that the rulemaking may severely circumscribe or even rescind Rule 14a-8. Such changes may include allowing state law or corporate bylaws to delineate whether and when a shareholder proposal would be included on the corporate proxy statement or even eliminating entirely the ability of shareholders to submit proposals for the corporate proxy statement. Moreover, Executive Order 14366 (issued December 11, 2025),[2] while focusing on the role of proxy advisors, also asked the SEC to evaluate curtailing environmental, social and governance shareholder proposals through an SEC rulemaking.

Rule 14a-8 creates value and manages risk for shareholders and their companies, and provides structural integrity for investor-company relationships.

The Commission has previously recognized in its July 2022 Proposing Release that:

The shareholder proposal process has become a cornerstone of engagement between shareholders and company management. Shareholder proposals provide an important mechanism for investors to express their views, provide feedback to companies, exercise oversight of management, and raise important issues for the consideration of their fellow shareholders in the company’s proxy statement. Moreover, investor support for shareholder proposal campaigns over the years has helped to shape many current corporate practices and policies, such as annual director elections, majority vote standards for director elections, and proxy access rights for shareholders.[3]

The petitioners believe that eliminating that cornerstone would destabilize corporate governance in America, removing a critical tool for board and management accountability to shareholders that investors rely upon in their investment and stewardship strategies.

The result would be the silencing of many shareholder proposals—and with them, lost value and risk management benefits—followed by an era of uncertainty and chaos in corporate governance, with more litigation, more opposition to director elections and pay packages, and a more adversarial relationship between investors and their companies.

The Commission has honed the Rule over the course of decades to balance the interests of issuers, proponents, and shareholders who vote on the proposals. The Commission should respect that balance, instead of upsetting market norms and expectations. This petition proposes modest adjustments to the shareholder proposal exclusion process to increase predictability and efficiency and limit demands on SEC staff resources. It also proposes that, if the SEC considers radical changes to the Rule, it first consider less harmful alternatives.

VI. The No-Action Process and Its 2026 Suspension

Since 1947, disputes over whether a proposal could be excluded have been addressed through the SEC’s no-action process. The process for staff consideration of shareholder proposal no-action requests was extensively described in the Commission’s 1976 release “Statement of Informal Proposals for the Rendering of Staff Advice with Respect to Shareholder Proposals.”[4]

When a company seeks to exclude a proposal, it submits a request to the SEC’s Division of Corporation Finance explaining the legal basis for doing so. Shareholder proponents may submit a response.

SEC staff then issue an informal no-action letter indicating whether or not they concur that the proposal may be excluded. Staff reasoning is typically brief often just a few sentences—either finding “some basis” for the company’s arguments and stating that the staff would not recommend enforcement action if the company excludes the proposal, or, if they disagree with the company’s arguments, stating that they are “unable to concur.” Staff need not address all bases for exclusion if they concur with the company on one. If staff concur, the company may omit the proposal from its proxy statement with a degree of regulatory assurance; if staff do not concur, most companies allow the proposal to proceed rather than risk enforcement action.

Only a court can definitively determine whether an exclusion is validly applied. Therefore, the informal staff opinions are nonbinding. Nevertheless, the shareholder proposal no-action process has historically provided a relatively fast and even-handed avenue for guiding company action and developing interpretive guidance under Rule 14a-8.

Provisions promulgated in Rule 14a-8 reinforce fairness in the conduct of this informal process:

Rule 14a-8(k) provides that the proponent “should try to submit any response to [the SEC staff], with a copy to the company, as soon as possible after the company makes its submission. This way, the Commission staff will have time to consider fully [proponent’s] submission before it issues its response.”

Rule 14a-8(g) provides that “Except as otherwise noted, the burden is on the company” to persuade the Commission or its staff that it is entitled to exclude a proposal.

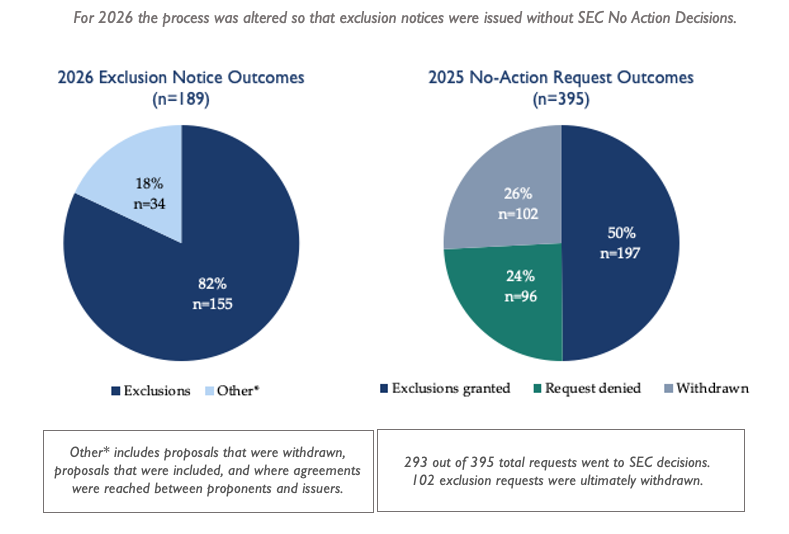

November 2025 Announcement

In November 2025, the SEC’s Division of Corporation Finance issued a statement announcing a policy applicable to the 2026 proxy season on how staff will assess and respond to company notifications under Rule 14a-8(j).[5] Under this policy, which was reportedly justified by a 2025 government shutdown that strained SEC staff resources, a company intending to exclude a shareholder proposal was still required to notify the Commission pursuant to Rule 14a-8(j), but the staff would not respond to the request or express any view on the company’s intended basis for exclusion. The Division reserved a single exception: where a company seeks to exclude a proposal under Rule 14a-8(i)(1) as an improper subject for shareholder action under state law.

To the extent that a company wanted a written response from the SEC regarding its exclusion notice, the policy provided for the staff to issue a letter, when requested by a company, stating that, based solely on the company’s or counsel’s unqualified representation and without evaluating its merits, it would not object to the omission of the proposal.

This no-objection process departed from the explicit terms of Rule 14a-8 in two distinct ways:

In issuing such “no objection” letters staff failed to accommodate and consider the proponent’s perspectives, a clear departure from the intent of Rule 14a-8(k);

The staff did not place the burden of persuasion on the company, instead accepting the company’s perspective without evaluating its persuasiveness, which is wholly inconsistent with Rule 14a-8(g).

Implementation of Rule 14a-8 by the Commission and the affected parties has historically depended on a combination of administrative oversight, evolving staff interpretation, and iterative dialogue between companies and investors. With the administrative layer removed during the 2026 proxy season interpretive authority shifted directly to issuers and the courts. Dispute resolution over exclusions migrated to litigation and market pressure.

An analysis of the impacts of withdrawing the no-action process during the 2026 proxy season demonstrated that the results were not neutral.[6] Instead:

Proposals were disadvantaged that sought to surface emerging issues such as the role and risks of AI because there was no applicable staff guidance for application by issuers and proponents.[7]

Proposals revised in form to comport with historical staff guidance on issues like micromanagement were not honored by receiving companies, leading to the exclusion of proposals that, in the normal course of the no-action process, would have been re-evaluated for consistency with the rules.

Issuers excluded proposals based on a risk assessment of whether they were likely to be subject to an injunctive suit by the proponent. In particular, issuers assessed that smaller shareholders with fewer resources were less likely to sue, rendering their proposals more easily excludable. Petitioners conclude that the abandonment of the no-action process was neither beneficial, in the public interest, nor consistent with the SEC’s mission to protect investors and maintain fair, orderly, and efficient markets.

Companies requested and received no-objection letters for proposals on topics for which the staff had consistently over the years refused to concur in a company’s analysis as a basis for exclusion, such as those relating to political spending.

Six lawsuits were filed by proponents seeking injunctive relief to include proposals on the proxy.

The suspension created chaos, not efficiency. Investors who had satisfied every requirement to file a proposal, but who lacked the litigation budget to fight for inclusion in court, were effectively silenced. Issuers fared no better: stripped of substantive SEC guidance, many chose the path of least resistance and included proposals they might have legitimately excluded, simply to avoid the litigation risk of guessing wrong.

The “no objection” letters that replaced substantive review made matters worse. They permitted companies to exclude proposals without presenting evidence (the exact opposite of what the Rule requires) while proponent submissions went unread. The Division’s policy did not merely or appropriately conserve staff resources dedicated to Rule 14a-8. In effect, it repealed a fundamental element of the rule.

Additionally, issuer behavior and outcomes from the most recent proxy season cannot be treated as determinative or predictive of how a permanent system lacking the no-action process would operate going forward. Companies this season were responding to a temporary suspension under conditions of considerable uncertainty; under an established regime without a neutral referee, issuers would likely grow far more aggressive in pursuing exclusions.

VII. Recommended Reforms to the Exclusion Notice Process

The suspension of the no-action process has highlighted areas in which the Rule can be improved for the benefit of both issuers and proponents—including encouraging the parties to resolve more of these disputes prior to SEC staff review. These improvements would reduce costs, ensure the Rule’s provisions are upheld, and restore an orderly, efficient no-action process.

This petition recommends technical reforms to ensure that Rule 14a-8 procedures and proposal exclusions align with the intentions of the Rule, provide clarity to the parties, and update the exclusion process to reflect common modern practices.

Our recommended changes (set forth in Appendix A) would accomplish the following refinements to the shareholder proposal exclusion process:

1. Modify the requirements for company submissions of exclusion notices.

a. Change the deadline for filing an exclusion notice from 80 to 90 days. Specify that this deadline must be calculated in advance of the company’s print deadline or proxy filing, whichever occurs earlier. This rectifies a problem that has emerged in recent years where the window for staff review of an exclusion request has been truncated by accelerated company deadlines for printing proxy statements which precede the formal date for submission of the proxy form for EDGAR.

b. Establish a mandatory two week engagement window for the proponent and issuer to seek a negotiated agreement in the two weeks after submission of the exclusion notice, potentially eliminating the need for a staff advisory opinion.

c. Guarantees that the staff advisory opinions issued after the engagement window continue to place the burden of persuasion squarely on the issuer to present concrete evidence supporting the excludability of the proposal. This procedural safeguard precludes the issuance of “no objection” letters based on the unqualified representations of issuers while ignoring rebuttal evidence from proponents.

2. Set clear timeframes for a proponent to respond if a company requests a staff advisory opinion:

a. Allow 14 business days for responses to procedural objections (such as proof of ownership) and 30 days for responses to substantive exclusions.

b. Reinforce that the staff must consider timely submitted proponent perspectives before issuing any advisory opinion.

3. Eliminate outdated paper copy submissions requirements:

a. Excise obsolete language in the existing Rule requiring the submission of six paper copies. This would reflect the modern reality that all submissions are now processed electronically.

In addition, to the extent that the Commission proposes rescinding the no-action process, we recommend that it consider less harmful alternatives, including our proposed refinements that would reduce the demands on staff time. Other less disruptive alternatives to reduce the resource demand of the no-action process have also been successfully deployed by the staff in prior instances and should be evaluated in lieu of outright rescission of the no-action process. Notably, from 2019 to 2022, the Division of Corporation Finance staff successfully utilized a summary tracking chart[8] to record its perspective on the excludability of individual shareholder proposals for which it had received exclusion notices, but only issuing no-action letters stating a rationale in a limited number of matters where the staff identified a pressing need to clarify a specific interpretive position. This and similar resource saving alternatives must be evaluated as viable options rather than revoking the highly valued no-action process entirely.

VIII. Alternatives to Eliminating the Substantive Framework and Procedures of Rule 14a-8

We are advised that the Commission may also, beyond revoking the no-action process, consider more severe changes to the shareholder proposal rule, such as deferring entirely to state law or corporate bylaws rather than maintaining consistent federal exclusions and procedures. Doing so would severely undermine this cornerstone of U.S. corporate governance, creating unacceptable regulatory uncertainty and litigation risk for both proponents and issuers, and create impediments for access to the Rule for smaller shareholders.

If the Commission issues such a proposed rulemaking rescinding or severely curtailing Rule 14a-8, we urge the Commission to also evaluate alternatives that maintain the federal rules while eliminating the no-action process. This evaluation should include consideration of whether the current rules provide sufficient clarity, or could be refined to be more objective to avoid the need for litigation. It should also consider the potential role of engagement to promote modification or withdrawal of proposals, which would reduce the need for the no-action process.

Outright rescission of Rule 14a-8 would upset a longstanding balance between investors and their companies built around the Rule’s exclusions and procedures for submitting shareholder proposals that appear on corporate proxy statements. For example, the relevance exclusion, Rule 14a-8(i)(5), considered and refined by the Commission over numerous administrations, screens for materiality to the specific issuer, relieving companies of an obligation to respond to, and protecting shareholders from consideration of, trivial or irrelevant proposals. The resubmission exclusion, Rule 14a-8(i)(12), considers the voting outcomes from the previous years and spares shareholders and the board from perennial re-litigation of proposals that have garnered only minimal support. The eligibility thresholds for filing proposals set the entry price, demanding a genuine and durable stake before the Rule may be invoked.

The Rules provide a low-cost and uniform mechanism for proposal access across every public company. Shareholders have an impressive record of deploying this process to elevate corporate consideration of substantial near and long-term risks. Shareholder proposals often raise critical issues that the board or management might otherwise neglect, helping to counteract the natural proclivity of corporate boards and managers to bury issues that could be of concern to investors. As financial economist Michael C. Jensen observed, corporate reporting and market communications are often shaped by incentives to meet or beat market expectations rather than to present a full account of risk.[9] Former SEC Chairman Arthur Levitt similarly warned in 1998 that the drive to satisfy earnings expectations could displace faithful representation with “a game of nods and winks.”[10] Management is often incentivized to short-term profit and setting strategy accordingly, while ignoring long-term risks. These concerns remain salient today, and shareholder proposals play an important role in counteracting positive spin or corporate concealment that can range from mere puffery to greenwashing and securities fraud.[11]

Proposals have called attention to company mismanagement and poor governance, warned of company-related financial collapses, public health crises, environmental failures, labor violations, failure to demonstrate that the interests of investors are being adequately considered and addressed. They have also successfully pushed to improve the governance of emerging technologies that will be central to the 21st century. In doing so, these shareholder proposals identified material risks that management had failed to adequately address before the ultimate costs to shareholders and the company became catastrophic and undeniable.[12]

Eliminating the Rule would harm investors and markets that rely upon consistent standards and procedures for placing proposals on proxies across public companies. It would inevitably create a Tower of Babel comprised of fragmented, conflicting filing and technical requirements spanning disparate state corporate laws and idiosyncratic company bylaws. Interpretation and enforcement would become entirely dependent on the slow, costly machinery of private litigation and evolving inconsistent judicial interpretations. This would suppress the availability of the proposal process and severely reduce transparency on material investor concerns. Costly litigation would permanently destabilize the established working relationships on which issuers and investors rely. Any rulemaking to significantly alter the Rule must fully account for the systemic harm inflicted on the market and exhaustively consider less harmful alternatives, as requested by this petition.

Conclusion

The right to file a shareholder proposal that appears on the corporate proxy statement is not a courtesy extended by management. It is a foundational aspect of corporate ownership. Shares carry voting rights, and under long-established corporate and federal frameworks, those voting rights have long included the ability to put hard questions—about strategy, risk, and disclosure—before fellow owners. Because these proposals are advisory, they do not overrule management. Instead, they inform it, pressure it, and aggregate the judgment of the people whose capital is at risk. This voice is also a source of market efficiency. Engaged owners surface information, press for crucial disclosures that let the whole market price risk more accurately, and discipline managers who would otherwise be insulated from accountability. Empirical evidence on shareholder engagement demonstrates that successful, well-targeted engagements lead to positive abnormal returns at targeted firms, while unsuccessful ones are not value-destructive.[13] Curtailing that voice weakens one of the few mechanisms through which dispersed owners can hold management to account.

The reforms in this petition are narrow, practical, and overdue and will protect a right that has stood for over 80 years. The Commission should adopt them and reject other ideas that would eliminate or harmfully modify this important SEC rule.

Sincerely,

Steven Rothstein

Chief Program Officer, Ceres

Dave Wallack

Executive Director, For the Long Term

Josh Zinner

Chief Executive Officer, Interfaith Center on Corporate Responsibility

Thomas P. DiNapoli

New York State Comptroller

Sanford Lewis

Director, Shareholder Rights Group

Bryan McGannon

Managing Director, US SIF

[1]https://www.reginfo.gov/public/do/eAgendaViewRule?pubId=202510&RIN=3235-AN47 (“The Division is considering recommending that the Commission propose rule amendments to modernize the requirements of Exchange Act Rule 14a-8 to reduce compliance burdens for registrants and account for developments since the rule was last amended.”).

[2]https://www.whitehouse.gov/presidential-actions/2025/12/protecting-american-investors-from-foreign-owned-and-politically-motivated-proxy-advisors/

[3] Substantial Implementation, Duplication, and Resubmission of Shareholder Proposals Under Exchange Act Rule 14a-8, Exchange Act Release No. 34-95267 (July 13, 2022), 87 Fed. Reg. 45,052 (proposed July 27, 2022).

[4] Statement of Informal Procedures for the Rendering of Staff Advice With Respect to Shareholder Proposals, Exchange Act Release No. 34-12599 (July 7, 1976), 41 Fed. Reg. 29,989 (July 20, 1976).

[5]https://www.sec.gov/newsroom/speeches-statements/statement-regarding-division-corporation-finances-role-exchange-act-rule-14a-8-process-current-proxy-season

[6]https://static1.squarespace.com/static/5d1f9923ca0f4800011d443a/t/69eff37e7fe4671d80fc6256/1777333118857/

SRG+Report+Final+04.27+%2B+website+link.pdf

[7]Id. at 13. Overall, 28% of exclusions in the 2025–2026 season asserted an (i)(7) ordinary business basis. In a majority of those—roughly 64%—companies excluded proposals even though prior SEC staff precedent did not clearly resolve whether exclusion was appropriate.

That 64% category is not uniform. It consists predominantly of two types of proposals that have historically required staff interpretation: (1) revised proposals that build on earlier models but modify language or scope, often to respond to prior SEC guidance or staff determinations on issues such as micromanagement, and (2) novel or innovative proposals that introduce new topics or structures not previously addressed by staff decisions.

[8]https://www.sec.gov/divisions/corpfin/shareholder-proposals-2019-2020.pdf

[9]https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1894304

[10]https://www.sec.gov/news/speech/speecharchive/1998/spch220.txt

[11]https://business.rice.edu/wisdom/companies-talk-more-clearly-when-business-booming

[12]https://www.iccr.org/reports/shareholder-proposals-an-essential-investor-right/

[13]https://www.researchgate.net/publication/253236822_Active_Ownership

Appendix A: Proposed Markup

(j) Question 10: What procedures must the company follow if it intends to exclude my proposal?

(1) If the company intends to exclude a proposal from its proxy materials, it must file its reasons with the Commission no later than 80 90 calendar days before the earlier of its print deadline or the date it files its definitive proxy statement and form of proxy with the Commission. The company must simultaneously provide you with a copy of its submission. The Commission staff may permit the company to make its submission later than 80 90 days before the company files its definitive proxy statement and form of proxy, if the company demonstrates good cause for missing the deadline.

(2) The company must file six paper copies of submit the following:

(i) The proposal;

(ii) An explanation of why the company believes that it may exclude the proposal, which should, if possible, refer to the most recent applicable authority, such as prior Division letters issued under the rule; and

(iii) A supporting opinion of counsel when such reasons are based on matters of state or foreign law.

The two calendar weeks after submission of a no-action request is considered the engagement period, in which the parties have an opportunity to engage and converge on an agreement for withdrawal of the no-action request.

If the engagement period ends without agreement, SEC staff may review the parties’ submissions and issue an advisory opinion—including but not limited to all instances in which the issuer and proponent have raised contested issues that require resolution.

(k) Question 11: May I submit my own statement to the Commission responding to the company’s arguments?

Yes, you may submit a response, but it is not required. The staff will consider your submission as well as the company’s. After the company makes its submission you should try to submit any response to us, with a copy to the company, within 14 business days of receipt of the exclusion notice for any procedural objection such as proof of ownership, and within 30 days to respond to any of the enumerated exclusions as soon as possibleafter the company makes its submission. This way, the Commission staff will have time to consider fully your submission before it issues its any response. You should submit six paper copies of your response.

Investor Coalition, NY Comptroller Petition SEC to Fix – Not Gut – Shareholder Proposal Rule

July 23, 2026

For media inquires please contact Esperanza@focalpointstrategygroup.com

Petition urges Commission to adopt practical reforms that streamline the no-action process and evaluate less disruptive alternatives before considering major changes to Rule 14a-8

WASHINGTON, D.C. — A coalition of investor groups and New York State Comptroller Thomas P. DiNapoli filed a rulemaking petition today urging the SEC to recalibrate, rather than dismantle, Rule 14a-8, the federal rule governing shareholder proposals on corporate proxy statements.

The petition responds directly to SEC Chairman Paul Atkins, who told the Society for Corporate Governance recently that this season's suspension of staff review of company arguments for excluding proposals cut resource demands and suggested he may make that suspension permanent. Atkins has also floated shifting shareholder proposal oversight to state law or company bylaws, and a White House Executive Order suggested SEC consideration of scrapping the rule outright.

The petitioners - DiNapoli, Ceres, the Interfaith Center on Corporate Responsibility, the Shareholder Rights Group, US SIF, and For the Long Term - argue that if the SEC is going to do a rulemaking, there's a more efficient fix that doesn't require abandoning investor protections.

Two core asks:

Streamline the proposal exclusion process before it reaches the SEC. The petition calls for a mandatory two-week engagement window after a company issues an exclusion notice, clear response deadlines for proponents, modestly extended filing windows, and an end to obsolete paper-filing requirements — changes meant to resolve more disputes privately and make SEC review faster when it is needed.

Require the SEC to test less drastic options first. Before rescinding the no-action process, handing oversight to state law, or otherwise gutting Rule 14a-8, the petition says the Commission is obligated under the Administrative Procedure Act to evaluate less harmful alternatives — including the procedural fixes above.

The petition cites this year's experience as the cautionary tale: with substantive no-action review suspended, costs didn't disappear, they moved — onto investors and companies navigating more uncertainty, inconsistent outcomes, and litigation. As the filing puts it: "The suspension created chaos, not efficiency."

Alongside the petition, investors also filed:

Citizen petitions with nearly 32,000 signatures opposing rescission of the rule

A FOIA request (Shareholder Rights Group and Democracy Forward) seeking records on the SEC's reported "previewing" of rulemaking plans with select constituencies

U.S. Senator Elizabeth Warren (D-MA): “Rescinding SEC Rule 14a-8 would be another giveaway to corporations and their executives at the expense of workers and retirees. From preventing shareholders from bringing lawsuits on company misconduct to rolling back disclosures key to investors, President Trump’s SEC seems more interested in stifling ordinary investors’ voices than protecting their rights.”

Sanford Lewis, Director, Shareholder Rights Group: "Good regulation starts with solving the right problem. If the Commission's objective is to reduce demands on staff resources, there are practical ways to accomplish that without abandoning a regulatory framework that has served investors, companies, and the markets for decades."

New York State Comptroller Thomas DiNapoli: "For more than eighty years, shareholder proposals have been a critical tool for investors to hold boards and management accountable. The right to include shareholder proposals on corporate proxies has driven reforms that strengthened American companies and protected shareholder value. Suspending the no-action process shifted costs onto investors and companies and fostered uncertainty, inconsistency, and litigation. We’re offering the SEC a better option: targeted fixes that ease the burden on staff while keeping a neutral referee on the field. That’s good for shareholders and good for the companies we invest in.”

Illinois State Treasurer Mike Frerichs: "Ultimately, weakening or taking away the shareholder proposal process is not going to make the sustainability risks for companies go away. It’s just going to make it harder for shareholders to raise them," Illinois State Treasurer Michael Frerichs said. "So naturally I am concerned that eliminating the 14a-8 process would reduce the rights of shareholders and limit our ability to engage companies facing material sustainability risks."

Dave Wallack, Executive Director, For the Long Term: "Long-term investors need functioning institutions. The choice before the SEC is not between efficiency and investor rights—it's between thoughtful modernization and unnecessary disruption. Before abandoning a framework that has served our capital markets for decades, the Commission should fully evaluate the practical, lower-cost alternatives already on the table."

The petition calls its recommendations "narrow, practical, and overdue," and comes as the SEC weighs potential Rule 14a-8 amendments on this year's agenda.

About For the Long Term

For the Long Term (FTLT) is a nonpartisan organization dedicated to strengthening the institutions, leaders, and policies that drive long-term economic growth and prosperity. FTLT works with state financial leaders, institutional investors, and market participants to advance practical solutions that promote long-term value creation, effective stewardship, and resilient capital markets. Through convenings, research, and strategic partnerships, FTLT helps public officials and investors navigate emerging challenges—from technological change and demographic shifts to corporate governance and economic competitiveness—while building the capacity of those entrusted with managing public resources. FTLT believes that strong institutions, informed leadership, and a long-term perspective are essential to ensuring that American markets remain the most dynamic, innovative, and trusted in the world.

Additional Quotes

“Our nation's capital markets system works best when investors and companies work together. The shareholder proposal process is an essential tool that allows investors to have direct dialogue with company management about material risks to the business. Rolling back this process will cause immense harm to our capital markets and will undermine investors' freedom to engage with the companies they own.” Andrew Collier, Senior Director, Freedom to Invest, Ceres. Phone: 202-774-0171. Email: acollier@ceres.org

About Ceres

For more than 35 years, Ceres has been at the forefront of building business leadership and supporting innovative market and policy solutions to address the world’s most pressing sustainability issues. We work with investors, companies, and policymakers to advance actions that reduce emissions and build a cleaner, more resilient economy – all in a way that advances justice and equity.

“ICCR has been deeply concerned about the ways this proposed attack on shareholder rights could impact our members and the wider landscape of corporate governance and accountability. These changes being suggested by the administration would undermine a tool that generations of Americans have come to depend upon to safeguard the long-term value and viability of their investments. At a time of growing unease about the condition and direction of the U.S. economy, Chair Atkins should be seeking to strengthen rather than undermine investor protections.” Josh Zinner, CEO, ICCR email: jzinner@iccr.org

About the Interfaith Center on Corporate Responsibility (ICCR)

The Interfaith Center on Corporate Responsibility (ICCR) is a broad coalition of more than 300 institutional investors collectively representing over $4 trillion in invested capital. ICCR members, a cross-section of faith-based investors, asset managers, pension funds, foundations, and other long-term institutional investors, have over 50 years of experience engaging with companies on environmental, social, and governance (“ESG”) issues that are critical to long-term value creation. ICCR members engage hundreds of corporations annually in an effort to foster greater corporate accountability. Visit our website www.iccr.org and follow us on LinkedIn, Bsky Social, and Facebook.

"Shareholder proposals help investors identify risks before they become larger problems. Making it harder for shareholders to question management does not make those risks disappear. It simply makes it harder for companies, boards, and investors to see them." Jonas Kron, Chief Advocacy Officer, Trillium Asset Management, LLC email:jkron@trilliuminvest.com

About Trillium Asset Management, LLC

Trillium Asset Management offers investment strategies and services that seek to advance humankind towards a global sustainable economy, a just society, and a better world. For over 40 years, the firm has been at the forefront of ESG thought leadership and draws from decades of experience focused exclusively on responsible investing. Devoted to aligning stakeholders’ values and objectives, Trillium combines impactful investment solutions with active ownership.

“Communication between investors and their portfolio companies is mutually beneficial. Restricting investors' ability to express their preferences directly —through filing or voting on shareholder proposals — will produce votes against directors that convey no clear or constructive signal to the companies." Elizabeth R. Levy, CFA, Managing Director, Clean Yield Asset Management email:liz@cleanyield.com

About Clean Yield Asset Management

For more than 40 years, Clean Yield Asset Management has used the power of investing to meet the financial goals of our clients while moving society toward a more just and sustainable future. Clean Yield works with individuals, families, family trusts, foundations, and aligned nonprofit clients to implement an investment strategy aligned with their progressive values. Our strategies ensure that our clients' investments are not only financially rewarding but also aligned with their values and contributing to a more sustainable world.

“The shareholder proposal process benefits the entire capital market value chain, not just proponents. Shareholder proposals are one of the few formal mechanisms investors have to raise material governance and risk issues directly with boards. The process is an efficient means to surface existing and emerging risks and increases transparency leading to better investment decision making.” Bryan McGannon, Managing Director of US Sustainable Investment Forum bmcgannon@ussif.org

US SIF Sustainable Investment Forum

They are the preeminent voice advancing sustainable investing. Members, who represent $5 trillion in assets under management or advisement, support US SIF’s mission to rapidly shift investment practices toward sustainability, focusing on long-term investment, the generation of positive social and environmental impacts and supporting the shift toward a more resilient and equitable planet and society. https://www.ussif.org

Governance Proposals Dominate the 2026 Proxy Season

These are highlights from an article posted by ISS-Corporate analyzing the 2026 season.

Shareholder Proposal Volume Falls to a Five-Year Low

Against these backdrops, the overall volume of shareholder proposals submitted and advanced to a vote has declined to a five-year low.

While the overall volume of proposal submissions and those appearing on the final ballot declined, governance-related proposals recorded an increase in overall volume. This relative resilience highlights the continued prioritization of core shareholder rights and board accountability mechanisms among investors as well as changes in proponents’ tactics.

In contrast, environmental and social proposals extended their downward trajectory with further declines in both the number of proposals submitted and proposals voted, reflecting a more selective investor approach toward these topics. Anti-ESG proposals, which had been rapidly increasing in volume, saw a decline as well, though they continue to comprise a meaningful portion of overall proposal volume.

The shift in proposal activity likely reflects a combination of factors, including the evolving political and regulatory landscape, the mixed success many environmental and social proposals have achieved in recent years, and the impacts of recent SEC actions.

Changes to the SEC’s shareholder proposal framework and no-action process appear to have altered the calculus for proponents, potentially discouraging some submissions while incentivizing others to pursue a more focused strategy. As a result, some proponents appear to have reduced proposal activity altogether, while others have become more selective in targeting issues and companies, or have redirected their efforts toward governance-related topics that historically receive broader shareholder support and face fewer ideological headwinds.

Taken together, these developments suggest that rather than signaling a diminished interest in environmental and social issues, the decline in proposal volume may reflect a strategic recalibration by proponents seeking to maximize impact and improve the likelihood of gaining meaningful shareholder backing.

ISS-Corporate’s Approach to Proxy Season Insight

The 2026 proxy season highlights significant changes in shareholder proposal activity. While overall proposal volume declined, governance-focused proposals remained resilient and continued to receive the strongest investor support, highlighting sustained shareholder focus on board accountability and shareholder rights. Meanwhile, environmental and social proponents appear to be recalibrating their tactics, adopting a more targeted approach.

As the 2026 proxy season concludes, these trends offer important signals about evolving investor priorities and the issues most likely to shape shareholder engagement and voting decisions in the years ahead. ISS-Corporate’s Compensation & Governance Advisory team helps companies analyze shareholder proposal trends, benchmark governance practices against market expectations, assess potential areas of shareholder concern, and develop engagement and disclosure strategies that align with investor priorities. Through data-driven insights and practical governance guidance, we support boards and management teams in preparing for future proxy seasons and strengthening shareholder relationships in an increasingly dynamic governance landscape.

Investors should be alarmed by the retreat of the Big Three asset managers from corporate stewardship

Andrew Behar, April 23, 2026

Not long ago, Larry Fink was writing annual letters to CEOs declaring that “climate risk is investment risk.” BlackRock, Vanguard, and State Street, the Big Three asset managers collectively controlling roughly $25 trillion, were telling corporate America that workforce diversity drives financial performance, that executive pay had to be tethered to long-term value, and that companies ignoring environmental risk were companies ignoring shareholder risk. That stance wasn’t altruism. It was investing logic grounded in deep research and fact.

That logic hasn’t changed. What changed is the political weather.

Under sustained pressure from state attorneys general, congressional threats, and an orchestrated anti-ESG campaign, the Big Three have systematically dismantled the very voting policies they spent years constructing. A new analysis of their 2026 proxy voting guidelines, compiled by Weil, Gotshal & Manges, reads like a before-and-after of institutional capitulation. The reversals are not subtle.

State Street’s policy no longer expects companies to disclose climate transition plans, emissions targets, Scope 3 data, or net-zero pathways. During engagement meetings, State Street now instructs itself to remain in “listen-only mode” during any discussion of climate targets.

BlackRock’s climate focus has narrowed from all companies to only those facing “material climate-related risks,” a loophole large enough to drive an oil tanker through. Vanguard has deleted the language requiring that board oversight failures on environmental and social risk trigger accountability votes against directors.

On workforce diversity, the retreat is equally stark. BlackRock no longer expects companies to disclose their approach to diversity, equity, and inclusion and has removed references to EEO-1 reporting as a baseline for workforce transparency. State Street, which famously placed the “Fearless Girl” statue in front of Wall Street’s Charging Bull, no longer expects any specific DEI disclosure and will not discuss diversity targets with companies.

Vanguard has excised “personal characteristics” like gender and race from its definition of board diversity altogether. These are not refinements. These are board-level decisions that will have negative financial consequences for their clients.

Systemic risk

The financial case for these commitments was never speculative. As You Sow’s research across 1,641 companies over five years demonstrated that greater workforce diversity correlates with outperformance on eight key financial measures: enterprise value growth rate, free cash flow per share, income after tax, long-term growth mean, 10-year price change, mean return on equity, return on invested capital, and 10-year total revenue compound annual growth rate. The data is not ideological. It is the kind of evidence-based analysis investors and asset managers are supposed to demand as a basic fiduciary responsibility, before allocating capital.

The Big Three are not merely asset managers. They are the largest shareholders in virtually every major publicly traded company in America. When they vote, they move markets. When they go silent on climate risk, they give corporate boards permission to look away. When they stop evaluating board diversity, they remove the single most effective mechanism shareholders have to hold boards accountable for the composition of their oversight function.

The downstream consequence falls not on the asset managers — they collect their fees either way — but on the underlying investors: pension funds, endowments, retail shareholders, retirees who cannot diversify away from systemic risk.

This is precisely the problem with surrendering long-term risk analysis to short-term political winds. Climate change does not operate on an election cycle. Extreme weather events, regulatory disruption, stranded assets, and supply chain fragility are not hypothetical future scenarios — they are present tense, priced into insurance markets, and showing up on balance sheets now. Boards that lack the expertise or mandate to oversee these risks are not just bad on governance grounds; they are expensive to own.

As You Sow’s own As You Vote 2026 Proxy Voting Guidelines take a different view of what responsible stewardship looks like. We continue to vote against directors who fail to set Paris-aligned net-zero targets. We oppose board slates lacking gender diversity below 40% female or racial diversity below 40% non-white. We vote against CEO pay that exceeds 100 times median worker pay, because the data shows that extreme pay disparity destabilizes corporate culture and distorts executive incentives away from long-term performance. We support transparent disclosure of political spending, because investors deserve to know whether their capital is financing lobbying that contradicts the company’s own stated strategy and values.

None of this is radical. It is the application of risk analysis, the fundamental job of any investor who intends to hold diversified portfolios over a horizon longer than the next quarterly earnings call.

The Big Three’s retreat will not go unnoticed by the companies they own. Corporate boards are watching, and the signal they are receiving is that the largest shareholders in the room have stood down. That is a signal that responsible investors, those who manage capital across decades, not news cycles, should consider very carefully.

Markets cannot price risk they refuse to measure. And stewards of capital who stop asking the questions do not stop bearing the consequences of the answers.

Even Musk Admirers Should Be Troubled by SpaceX’s Governance

Posted by Lucian Bebchuk (Harvard Law School) and Kobi Kastiel (Tel Aviv University), on Tuesday, June 2, 2026

This is an excerpt from an article posted on the Harvard Law School Forum on Corporate Governance.

SpaceX is planning to go public in mid-June with a governance structure that would free Elon Musk from constraints on his power. Many investors regard Musk’s talents so highly that they might be willing to overlook this lack of constraints. In their view, freeing Musk from constraints would not be a bug but a beneficial feature. However, the loosening of constraints on Musk’s power should be viewed as troublesome even by his most fervent admirers.

(We wrote a post earlier about this subject based on media reports published prior to the release of the SpaceX prospectus. Now that the prospectus has been released, the discussion below updates and further develops our earlier critique.)

To understand the governance problems of SpaceX, it is important to distinguish among different types of investor beliefs about Musk. One set of investors views Musk as having the best ability to maximize the size of the SpaceX pie (that is, the total value that the company will generate to be shared among its shareholders). Such investors might favor governance provisions that would enable Musk to set company strategy with minimal interference from outsiders.

However, there are at least four aspects of the IPO structure that should nonetheless trouble these Musk admirers. First, a belief that Musk knows best how to maximize the pie does not necessarily imply any belief about how Musk would split that pie between public investors and himself.

A major role of corporate rules and governance arrangements in public companies is to constrain the extent to which insiders can split the pie in their favor. The design of the SpaceX IPO — namely, the company’s incorporation in Texas combined with the wide array of provisions in its charter — would give Musk expansive freedom not only to set the company’s strategy as he sees fit but also to allocate the pie as he wishes.

Among other things, Musk would be free (by an explicit provision of the charter) to take for himself any business opportunities presented to SpaceX. He would also be able to arrange related-party transactions that would benefit himself at the expense of public investors, sell himself a large fraction of SpaceX’s assets at a favorable price, and secure giant pay awards. Musk would be able to make such decisions in ways that would confer very large private benefits on him; he would then obtain a substantially disproportionate slice of the pie, leaving public investors with considerably less than their pro rata share.

Second, a strong belief that Musk is by far the best leader for SpaceX now and in the coming years does not imply that he will remain so forever. The pages of business history are full of individuals who were at the very top of their game at one time but later turned subpar and value-destroying.

Accordingly, even the most fervent fans of Musk should worry that Musk’s control is so deeply hard-wired into the SpaceX structure. Can they be certain that Musk, who is 54, will still be a fitting leader at 74 or 84? And if he were to pass away, or become incapacitated or incompetent, control would presumably pass to his heirs or to those managing the trusts through which he holds his superior-voting shares. The prospectus does not disclose who these individuals are, making any assessment of this risk difficult.

Third, even if Musk were to remain the most fitting leader for decades, his incentives would matter. For any given leader, performance could be affected substantially by how closely his interests align with those of public investors. It is therefore important to recognize that the SpaceX structure would enable Musk to cash out any fraction of his equity stake without weakening his lock on control. If Musk were to move to a small-minority controller structure, public investors would be significantly harmed. (For a detailed analysis of the value-reducing costs associated with such a structure, see our article The Perils of Small-Minority Controllers.)

Fourth, no matter how exceptional a leader is believed to be, his performance will likely depend on the time and attention he devotes. At Tesla, despite Musk’s massive pay package, he was not required to limit his outside activities or commit any specific amount of time and attention to the company. Musk took advantage of that freedom by spending substantial time away from Tesla during the months in which he focused on the Twitter acquisition and subsequently on leading DOGE. Importantly, although the IPO design of SpaceX includes an ironclad commitment not to remove Musk from the CEO and Chair positions, Musk would be entirely free to choose how much time and effort to spend elsewhere.

Of course, none of these risks is certain to materialize. But they are all serious risks. Even investors who believe that Musk walks on water should give these risks significant weight when assessing how much they are willing to pay for SpaceX shares.

Defend Shareholder Rights: A Citizens Petition

Promoted by Shareholder Rights Group, Interfaith Center on Corporate Responsibility, Friends of the Earth, Green America, and Public Citizen

Endorsed by 19,245 Individuals or Organizations as of July 20, 2026

To: Securities and Exchange Commission

Dear Chairman Atkins and Commissioners Peirce and Uyeda,

We write as retirees, pension beneficiaries, and individual and institutional investors whose savings depend on the integrity of America's capital markets. We urge you to preserve the shareholder proposal rule as a cornerstone of property rights and free-market accountability.

Shareholder proposals are an expression of ownership. For eighty years, the ability of shareholders to raise questions before the companies they own has been one of the most effective free market-based checks on corporate mismanagement. The need for regulators to intervene is reduced when owners can speak directly. That is the genius of the system — and precisely what is at risk.

Shareholders have advanced sound governance of their companies through decades of governance reforms, adopted first through the shareholder proposal process and then as general market practice.

When investors ask a clothing retailer to account for supply chain vulnerabilities, they are protecting brand equity and long-term profitability. When they ask a pharmaceutical company to address legislative risk embedded in its earnings guidance, they are doing the analytical work that sound investing requires. When they flag water scarcity exposure for agricultural, beverage, semiconductor, or mining companies, they are surfacing risks that conventional financial filings routinely omit — risks that eventually become losses borne by ordinary shareholders.

Other investors have a right to inquire whether environmental or social commitments of a company are undercutting shorter term profitability. Regardless of the time horizons of investing, this is a critical right of investors to engage a fundamental American value — the marketplace of ideas.

If the shareholder proposal process is curtailed, the practical result is not quieter markets. It is a transfer of power: away from diverse owners, and toward a narrow class of the largest institutional players. Smaller investors — retirees, pension funds, individual savers — will lose one of the only shareholder protection tools scaled to their resources. Blind spots will accumulate. Risks that could have been surfaced early will compound, spreading across companies and sectors until they become systemic.

The boards and executives of public companies should answer to their owners. That principle is not progressive or conservative — it is foundational to capitalism.

We urge the Commission to honor its mandate to protect investors and maintain fair, efficient markets by keeping this rule intact.

Let America's public companies be guided by their shareholders — not shielded from them.

This petition is sponsored by investment organizations: Interfaith Center on Corporate Responsibility, the Shareholder Rights Group, US/SIF, Freedom to Invest and For the Long-Term.

Shareholder Proposals and Corporate Governance in a Season of Regulatory Uncertainty

Access the full text here.

Executive Summary

In the 2026 proxy season, the Securities and Exchange Commission (SEC) Division of Corporation Finance upended a long-standing practice of issuing informal decisions on whether shareholder proposals are excludable by the companies receiving them.

Although the SEC shareholder proposal rule, Rule 14a-8, remained in force, the SEC’s administrative dispute resolution mechanism—neutral staff review through the no-action process—was gone. The Division cited resource constraints and the sufficiency of existing guidance to justify suspending the no-action process for the current proxy season. As it stated on November 17, “due to current resource and timing considerations… as well as the extensive body of guidance from the Commission and the staff available to both companies and proponents… the Division has determined to not respond to no-action requests…” How did these changes affect the ability of shareholders to use the proposal process to raise potentially material issues with their companies and fellow shareholders? How did the SEC’s absence as a neutral arbiter of exclusion claims affect how issuers and proponents behaved? How did it affect the efficiency and effectiveness of the shareholder proposal process as a means of placing important questions before shareholders on corporate proxy statements? This analysis examines how the shareholder proposal process functioned during the 2025–2026 proxy season to identify patterns in how companies and shareholders navigated the process in the absence of routine staff review, to assess issues of fairness, balance, and efficiency and to make recommendations based on the lessons from the season.

The data indicate a chilling effect on both proponents and issuers. Shareholders filed approximately 20% fewer proposals for the 2026 season. Companies filed over 100 fewer exclusion notices.

Many companies, it seems, made a prudent judgment: without SEC staff guidance on individual proposals, unilateral exclusion carried too much risk, including proponent litigation, reputational risk, potential fuel for a proxy fight over director elections, and other concerns. Rather than exploit the absence of oversight, many companies receiving proposals let the proposals go to the proxy, sometimes even explicitly citing the lack of SEC guidance as their reason for including proposals they believed might otherwise be excludable. Other companies similarly situated engaged with proponents to produce settlement agreements.

The rate at which proposals were excluded by companies in proportion to the number of proposals filed, in the absence of the SEC’s informal determinations, was similar to the rate excluded last year after SEC determinations. Yet, analysis of these exclusions revealed several important trends.

Comparison of 2025 and 2026 Process Outcomes

One of most common justifications for excluding proposals was the ordinary business rule—a determination that typically turns on subjective factors and has historically benefited from substantive SEC staff evaluation. Unfortunately, the largest portion of these exclusions clearly disadvantaged proponents who were either filing proposals on emerging risks on which staff had not previously opined or had refined a prior proposal’s language to address prior SEC staff concerns about prescriptive language. In both categories, the absence of SEC involvement undermined an orderly process and fair resolution of disputes over excludability, allowing exclusions to proceed despite the lack of staff guidance.

This exclusion trend is particularly troubling for proposals addressing an issue on which the staff has never opined. Even if the proposal concerned a significant emerging risk, exclusion could proceed despite the lack of staff guidance.

For example, at proposal at Amazon requesting company-specific disclosure of workforce risks tied to evolving U.S. immigration policy was excluded despite the absence of prior staff guidance on the topic. Proponents sought analysis of how recent and anticipated changes to immigration rules—particularly those affecting H-1B visa holders, warehouse labor, and truck drivers—could disrupt workforce, logistics capacity, and operating costs. Given the scale of Amazon’s workforce and reliance on these labor segments, this is an issue that a reasonable investor could view as financially material and decision-useful, yet the proposal was excluded without the benefit of any staff position addressing similar subject matter.

Similarly, on a year-to-year basis, the SEC sends signals to proponents and issuers regarding whether proposal language is too prescriptive, allowing proponents to revise proposals accordingly. This iterative feedback loop aligns proposal drafting with evolving staff interpretations. However, in the 2026 proxy season, such revisions were not ratified by staff review. As a result, issuers exercised unilateral discretion, and even proposals that may have been revised in good faith to conform with prior SEC guidance were nevertheless excluded.

For example, at AbbVie Inc., shareholders requested that the board oversee human rights due diligence to produce an impact assessment identifying actual and potential adverse human rights impacts in the company’s operations and supply chain, including effects on the right to health. Notably, this proposal appears to have been drafted to be less prescriptive than a prior 2025 proposal seeking a human rights impact assessment submitted to Eli Lilly, which the staff had permitted to be excluded on micromanagement grounds. The Eli Lilly proposal explicitly mandated the assessment cover “operations, activities, business relationships, and products”. By contrast, the AbbVie proposal narrowed and generalized the request—focusing on board oversight and an impact assessment framework rather than dictating exhaustive coverage parameters. Despite this apparent effort to align with prior staff reasoning and reduce prescriptiveness, AbbVie relied on the earlier Eli Lilly determination to justify exclusion. This illustrates how, in the absence of updated staff review, even materially revised proposals that address prior deficiencies can be excluded based on inapposite precedent.

Thus, an analysis of the ordinary business exclusions reveals that exclusions during this season disproportionately blocked (i) proposals addressing emerging issues lacking precedent and (ii) proposals that had undergone compliance-oriented revisions based on prior staff signals. The absence of no-action letters was therefore not neutral—it both impeded shareholders’ ability to surface new, financially relevant risks and disrupted the established corrective process that typically refines proposal language over time.

In another significant portion of exclusions, the companies claimed that their own activities substantially implemented the proposal. SEC staff is better positioned to provide a neutral evaluation of whether the company activities go as far as a proposal requests. These determinations are not appropriately left to the issuers.

Technical grounds—such as providing inadequate documentation that the proponent owned the necessary shares, or missing filing deadlines—accounted for another meaningful portion of exclusions. Some of these deficiencies seemed clear-cut. But without a structured opportunity for proponents to respond, questions remained about whether some of these technical exclusions rested on incomplete or disputed records that SEC staff would historically have scrutinized.

The disappearance of routine administrative review also caused at least six proponents to bring their disputes into federal court. Three of these cases resolved quickly after the companies agreed to include the proposals or provide the requested disclosure. These cases underscore how, in the absence of staff intermediation, formal legal action began to substitute for what had previously been an administrative and negotiated process. As proponent driven litigation became the primary enforcement mechanism for Rule 14a-8, a structural imbalance also took shape: the ability to defend a proposal increasingly depended on having the financial and legal resources to sue, in contradiction of the rule’s share ownership thresholds—which were designed to give even modest Main Street shareholders a voice.

This shift reflects a broader reconfiguration of how the rule operates in practice. Rule 14a-8 has historically depended on a combination of administrative oversight, evolving staff interpretation, and iterative dialogue between companies and investors. When the administrative layer was removed, interpretive authority shifted to issuers, and dispute resolution migrated to litigation and market pressure.

In that environment, the dynamics between proponents and companies changed materially. Proponents—who typically seek collaborative engagement with the company and dialogue with fellow shareholders—were forced into a position where they must consider escalation, including litigation, to ensure inclusion of proposals on the proxy.

The report concludes with five key recommendations for strengthening Rule 14a-8 and the shareholder proposal framework:

Preserve Rule 14a-8. The shareholder proposal mechanism is a vital communication channel between investors and corporate management. Weakening or eliminating it would undermine shareholders’ ability to raise governance concerns and hold management accountable.

Restore the no-action process. The SEC should revive its administrative process for resolving proposal exclusion disputes. Without it, conflicts are pushed into costly federal litigation or contentious shareholder campaigns. Some streamlining is possible for clear-cut procedural defects, but contested or fact-dependent claims still require meaningful staff review.

Eliminate “no-objection” letters. The practice of issuing no objection letters based solely on a company’s own unverified representations is inconsistent with Rule 14a-8’s intent. It implies administrative endorsement of unilateral exclusions regardless of consistency with the rule, and should be discontinued.

Issue clearer, more objective guidance. While appropriately restoring clarity about ensuring that proposals are relevant to the companies receiving them, Staff Legal Bulletin 14M also introduced excessive subjectivity into key exclusion determinations—particularly on “ordinary business” and “micromanagement” grounds. The subjective criteria provide staff with too much discretion; returning to more objective standards would improve predictability and reduce the need for repeated case-by-case adjudication.

Protect smaller shareholders’ access. Any reforms should ensure the process remains accessible to individual investors and smaller asset managers, who are unlikely to pursue litigation and who have historically filed some of the most important proposals on potentially material issues for their companies.

The 2025–2026 proxy season ultimately demonstrates both the resilience and the fragility of the shareholder proposal system. Shareholders kept raising concerns about governance, risk oversight, and corporate conduct. Some companies kept engaging constructively. But the absence of consistent regulatory oversight has introduced uncertainty, uneven outcomes, and shifted investor-company relations onto a more adversarial footing, dependent on litigation and escalatory tactics, rather than orderly SEC staff assessment of whether a proposal is consistent with the rule.

Preserving Shareholder Rights Protects Workers, Retirees, and the Integrity of American Capital Markets

March 26, 2026

Posted by Elizabeth Steiner, Oregon State Treasurer

Securities and Exchange Commission (SEC) Chair Paul Atkins recently reiterated his preference to loosen corporate accountability standards at a conference hosted by the Council of Institutional Investors. As the fiduciary for a state pension fund, I believe that weakening shareholder engagement creates risks that beneficiaries and state governments cannot afford.

Stories of CEOs raking in multimillion-dollar bonuses while middle-class workers struggle to pay rent or save for retirement have become all too familiar. Those disparities didn’t arise overnight but they have sharpened investor and public scrutiny of corporate governance. That’s why the federal administration’s effort to weaken shareholder rights is so concerning. Shareholders must have a voice in corporate governance given the capital they have invested in American businesses.

As Oregon State Treasurer I am charged with managing a diversified institutional portfolio of more than $148 billion in assets under management, including the Oregon Public Employees Retirement Fund (OPERF), one of the largest public pension funds in the country. Treasury staff invest these assets to achieve strong, risk-adjusted returns for beneficiaries. Public employees’ and retirees’ financial security depends on the long-term health of the assets we help steward.

We take our shareholder stewardship role seriously. During the 2024 proxy voting season Oregon Treasury voted in 5,333 meetings on over 50,305 individual items. The proxy votes we cast and the shareholder rights that underpin them are tools we use every year in service of the workers and retirees whose money is entrusted to us.

In December I urged SEC Chair Paul Atkins to reconsider recent SEC changes that restrict shareholder rights. In a letter co-signed by half a dozen state financial officers, we warned Chair Atkins that changes to the long-standing processes that protect shareholders would “suppress shareholder governance, diminish corporate transparency and accountability, and create risks to profitability and reputation for companies—further undermining the confidence that has attracted global investors to American firms and markets.”

Thanks to the efforts of shareholders, most S&P 500 companies now publish environmental, social, and governance disclosures that investors use to understand long-term risk and strategy. For example, shareholder engagement has codified “say on pay” votes. It has encouraged wider adoption of independent board leadership and strengthened oversight practices improving accountability for long-term investors. It has prompted hundreds of companies to disclose political spending with corporate funds and data on sustainability efforts.

For large institutional investors such as OPERF these votes are about value. Pension funds, asset managers, and other institutional investors representing millions of workers and retirees — including those whose pensions and savings we manage here in Oregon — advance governance improvements because these activities directly affect risk and value over decades.